Advertisement

We Think Batu Kawan Berhad's (KLSE:BKAWAN) CEO Compensation Package Needs To Be Put Under A Microscope

Key Insights

- Batu Kawan Berhad to hold its Annual General Meeting on 28th of February

- Total pay for CEO Hau-Hian Lee includes RM4.38m salary

- The total compensation is 908% higher than the average for the industry

- Batu Kawan Berhad's EPS declined by 36% over the past three years while total shareholder loss over the past three years was 14%

Batu Kawan Berhad (KLSE:BKAWAN) has not performed well recently and CEO Hau-Hian Lee will probably need to up their game. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 28th of February. They will also get a chance to influence managerial decision-making through voting on resolutions such as executive remuneration, which may impact firm value in the future. We present the case why we think CEO compensation is out of sync with company performance.

See our latest analysis for Batu Kawan Berhad

Comparing Batu Kawan Berhad's CEO Compensation With The Industry

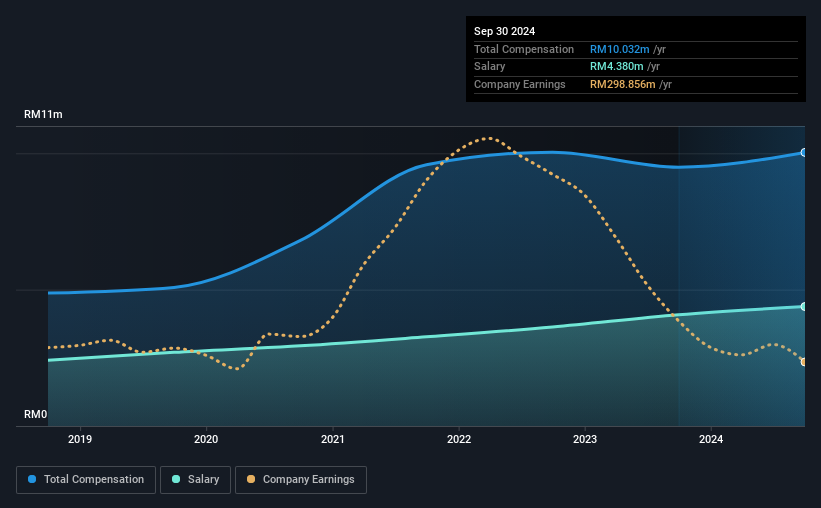

According to our data, Batu Kawan Berhad has a market capitalization of RM7.6b, and paid its CEO total annual compensation worth RM10m over the year to September 2024. That's a modest increase of 5.7% on the prior year. We think total compensation is more important but our data shows that the CEO salary is lower, at RM4.4m.

In comparison with other companies in the Malaysian Chemicals industry with market capitalizations ranging from RM4.4b to RM14b, the reported median CEO total compensation was RM995k. Hence, we can conclude that Hau-Hian Lee is remunerated higher than the industry median. Moreover, Hau-Hian Lee also holds RM31m worth of Batu Kawan Berhad stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | RM4.4m | RM4.1m | 44% |

| Other | RM5.7m | RM5.4m | 56% |

| Total Compensation | RM10m | RM9.5m | 100% |

On an industry level, roughly 60% of total compensation represents salary and 40% is other remuneration. In Batu Kawan Berhad's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Batu Kawan Berhad's Growth

Batu Kawan Berhad has reduced its earnings per share by 36% a year over the last three years. Its revenue is down 6.5% over the previous year.

Few shareholders would be pleased to read that EPS have declined. This is compounded by the fact revenue is actually down on last year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Batu Kawan Berhad Been A Good Investment?

With a three year total loss of 14% for the shareholders, Batu Kawan Berhad would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

CEO pay is simply one of the many factors that need to be considered while examining business performance. In our study, we found 3 warning signs for Batu Kawan Berhad you should be aware of, and 1 of them is a bit unpleasant.

Important note: Batu Kawan Berhad is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Batu Kawan Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:BKAWAN

Batu Kawan Berhad

An investment holding company, cultivates and processes palm and rubber products in Malaysia, the Far East, the Middle East, South East Asia, Southern Asia, Europe, North and South America, Australia, Africa, and internationally.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

956 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative