Syarikat Takaful Malaysia Keluarga Berhad's (KLSE:TAKAFUL) CEO Compensation Is Looking A Bit Stretched At The Moment

Key Insights

- Syarikat Takaful Malaysia Keluarga Berhad will host its Annual General Meeting on 21st of May

- Salary of RM1.32m is part of CEO Nor Zainal's total remuneration

- The total compensation is 101% higher than the average for the industry

- Syarikat Takaful Malaysia Keluarga Berhad's EPS declined by 4.3% over the past three years while total shareholder return over the past three years was 17%

CEO Nor Zainal has done a decent job of delivering relatively good performance at Syarikat Takaful Malaysia Keluarga Berhad (KLSE:TAKAFUL) recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 21st of May. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

See our latest analysis for Syarikat Takaful Malaysia Keluarga Berhad

Comparing Syarikat Takaful Malaysia Keluarga Berhad's CEO Compensation With The Industry

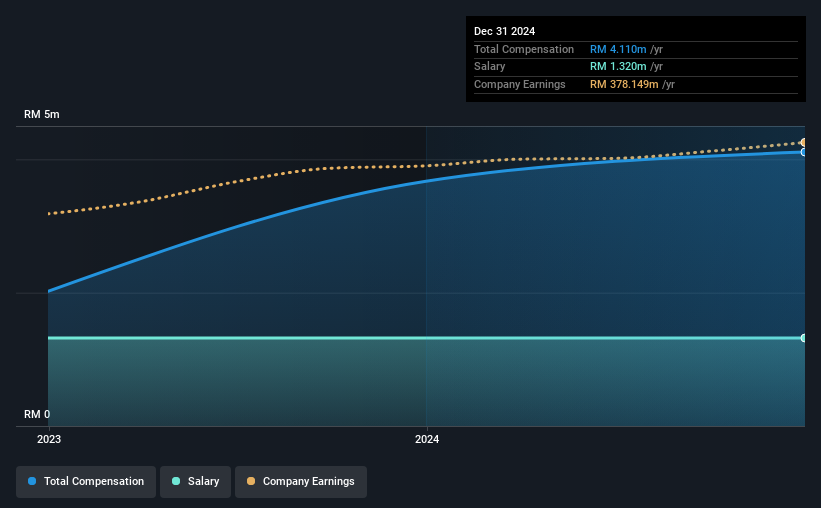

According to our data, Syarikat Takaful Malaysia Keluarga Berhad has a market capitalization of RM3.1b, and paid its CEO total annual compensation worth RM4.1m over the year to December 2024. That's a notable increase of 12% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at RM1.3m.

On examining similar-sized companies in the Malaysian Insurance industry with market capitalizations between RM1.7b and RM6.9b, we discovered that the median CEO total compensation of that group was RM2.0m. This suggests that Nor Zainal is paid more than the median for the industry.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | RM1.3m | RM1.3m | 32% |

| Other | RM2.8m | RM2.4m | 68% |

| Total Compensation | RM4.1m | RM3.7m | 100% |

On an industry level, around 78% of total compensation represents salary and 22% is other remuneration. In Syarikat Takaful Malaysia Keluarga Berhad's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Syarikat Takaful Malaysia Keluarga Berhad's Growth Numbers

Syarikat Takaful Malaysia Keluarga Berhad has reduced its earnings per share by 4.3% a year over the last three years. In the last year, its revenue is up 20%.

The decrease in EPS could be a concern for some investors. But on the other hand, revenue growth is strong, suggesting a brighter future. It's hard to reach a conclusion about business performance right now. This may be one to watch. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Syarikat Takaful Malaysia Keluarga Berhad Been A Good Investment?

Syarikat Takaful Malaysia Keluarga Berhad has generated a total shareholder return of 17% over three years, so most shareholders would be reasonably content. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

In Summary...

The overall company performance has been commendable, however there are still areas for improvement. Until EPS growth picks back up, we think shareholders may find it hard to justify increasing CEO pay given that they are already paid above industry average.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We identified 2 warning signs for Syarikat Takaful Malaysia Keluarga Berhad (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you're looking to trade Syarikat Takaful Malaysia Keluarga Berhad, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TAKAFUL

Syarikat Takaful Malaysia Keluarga Berhad

Manages family and general takaful businesses in Malaysia and Indonesia.

Undervalued with excellent balance sheet.

Market Insights

Community Narratives