- Malaysia

- /

- Healthcare Services

- /

- KLSE:PHARMA

There's No Escaping Pharmaniaga Berhad's (KLSE:PHARMA) Muted Revenues

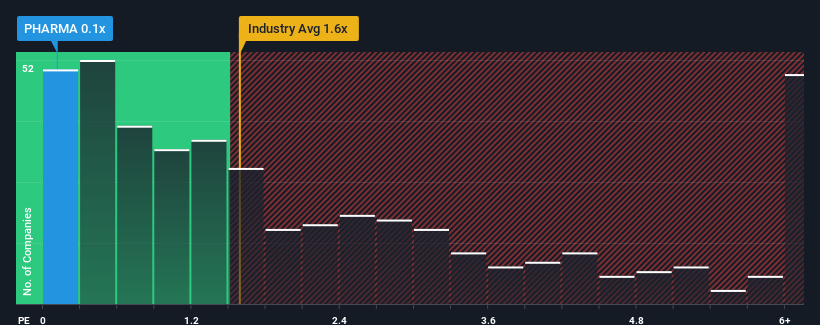

Pharmaniaga Berhad's (KLSE:PHARMA) price-to-sales (or "P/S") ratio of 0.1x may look like a very appealing investment opportunity when you consider close to half the companies in the Healthcare industry in Malaysia have P/S ratios greater than 2.9x. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Pharmaniaga Berhad

What Does Pharmaniaga Berhad's P/S Mean For Shareholders?

Pharmaniaga Berhad could be doing better as it's been growing revenue less than most other companies lately. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Pharmaniaga Berhad.Is There Any Revenue Growth Forecasted For Pharmaniaga Berhad?

Pharmaniaga Berhad's P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Retrospectively, the last year delivered a decent 4.2% gain to the company's revenues. However, this wasn't enough as the latest three year period has seen an unpleasant 24% overall drop in revenue. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 1.8% as estimated by the sole analyst watching the company. Meanwhile, the broader industry is forecast to expand by 8.1%, which paints a poor picture.

With this in consideration, we find it intriguing that Pharmaniaga Berhad's P/S is closely matching its industry peers. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Final Word

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Pharmaniaga Berhad's analyst forecasts revealed that its outlook for shrinking revenue is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless there's material change, it's hard to envision a situation where the stock price will rise drastically.

You need to take note of risks, for example - Pharmaniaga Berhad has 4 warning signs (and 3 which are a bit concerning) we think you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:PHARMA

Pharmaniaga Berhad

An investment holding company, operates as an integrated healthcare service provider in Malaysia, Indonesia, and internationally.

Slight and fair value.

Market Insights

Community Narratives