Advertisement

- Malaysia

- /

- Medical Equipment

- /

- KLSE:ONEGLOVE

Shareholders Will Probably Not Have Any Issues With One Glove Group Berhad's (KLSE:ONEGLOVE) CEO Compensation

Key Insights

- One Glove Group Berhad's Annual General Meeting to take place on 2nd of September

- Total pay for CEO BT Low includes RM540.0k salary

- The total compensation is 31% less than the average for the industry

- One Glove Group Berhad's EPS declined by 51% over the past three years while total shareholder loss over the past three years was 90%

The performance at One Glove Group Berhad (KLSE:ONEGLOVE) has been rather lacklustre of late and shareholders may be wondering what CEO BT Low is planning to do about this. At the next AGM coming up on 2nd of September, they can influence managerial decision making through voting on resolutions, including executive remuneration. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We have prepared some analysis below to show that CEO compensation looks to be reasonable.

View our latest analysis for One Glove Group Berhad

Comparing One Glove Group Berhad's CEO Compensation With The Industry

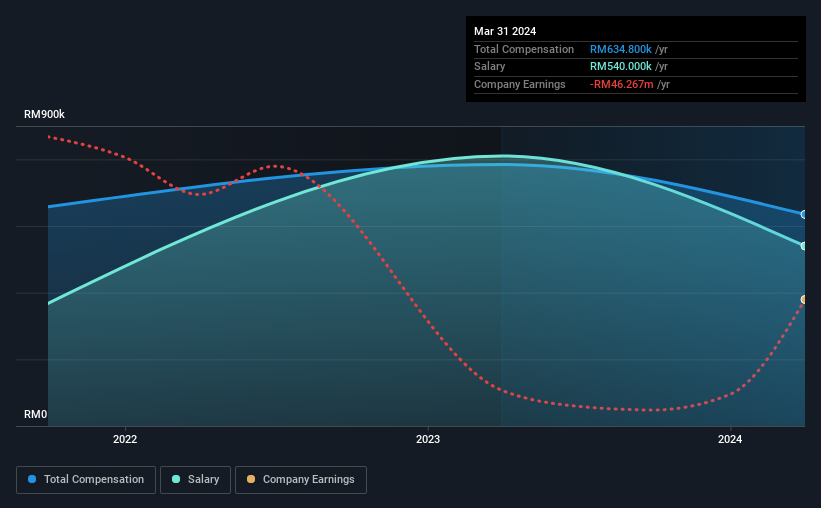

Our data indicates that One Glove Group Berhad has a market capitalization of RM111m, and total annual CEO compensation was reported as RM635k for the year to March 2024. That's a notable decrease of 19% on last year. In particular, the salary of RM540.0k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the Malaysia Medical Equipment industry with market capitalizations below RM875m, reported a median total CEO compensation of RM916k. Accordingly, One Glove Group Berhad pays its CEO under the industry median. Moreover, BT Low also holds RM40m worth of One Glove Group Berhad stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | RM540k | RM810k | 85% |

| Other | RM95k | 15% | |

| Total Compensation | RM635k | RM785k | 100% |

On an industry level, around 74% of total compensation represents salary and 26% is other remuneration. It's interesting to note that One Glove Group Berhad pays out a greater portion of remuneration through salary, compared to the industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

One Glove Group Berhad's Growth

Over the last three years, One Glove Group Berhad has shrunk its earnings per share by 51% per year. In the last year, its revenue is up 566%.

The reduction in EPS, over three years, is arguably concerning. But in contrast the revenue growth is strong, suggesting future potential for EPS growth. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has One Glove Group Berhad Been A Good Investment?

Few One Glove Group Berhad shareholders would feel satisfied with the return of -90% over three years. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

The fact that shareholders are sitting on a loss is certainly disheartening. The downward trend in share price performance may be attributable to the the fact that earnings growth has gone backwards. In the upcoming AGM, shareholders will get the opportunity to discuss these concerns with the board and assess if the board's plan is likely to improve company performance.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 4 warning signs for One Glove Group Berhad (2 can't be ignored!) that you should be aware of before investing here.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:ONEGLOVE

One Glove Group Berhad

An investment holding company, manufactures, markets, and sells examination gloves and other related activities in Malaysia, Japan, Germany, the United States, India, and internationally.

Low risk and overvalued.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$245.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RA

RacerBVN on iShares Trust - iShares Preferred and Income Securities ETF ·

This one is all about the tax benefits

Fair Value:US$54.5543.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FatPie on SoFi Technologies ·

Estimated Share Price is $79.54 using the Buffett Value Calculation

Fair Value:US$79.5465.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3925.9% undervalued

961 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative