Yenher Holdings Berhad's (KLSE:YENHER) 27% Price Boost Is Out Of Tune With Earnings

Yenher Holdings Berhad (KLSE:YENHER) shareholders have had their patience rewarded with a 27% share price jump in the last month. Looking further back, the 22% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

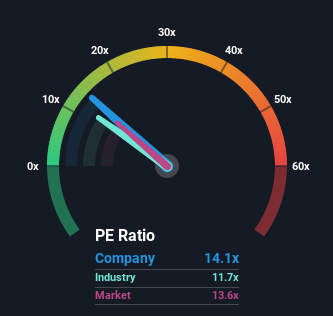

In spite of the firm bounce in price, it's still not a stretch to say that Yenher Holdings Berhad's price-to-earnings (or "P/E") ratio of 14.1x right now seems quite "middle-of-the-road" compared to the market in Malaysia, where the median P/E ratio is around 14x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

The recent earnings growth at Yenher Holdings Berhad would have to be considered satisfactory if not spectacular. It might be that many expect the respectable earnings performance to only match most other companies over the coming period, which has kept the P/E from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

See our latest analysis for Yenher Holdings Berhad

Does Growth Match The P/E?

The only time you'd be comfortable seeing a P/E like Yenher Holdings Berhad's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered a decent 6.9% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen an unpleasant 12% overall drop in EPS. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Comparing that to the market, which is predicted to deliver 8.5% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

With this information, we find it concerning that Yenher Holdings Berhad is trading at a fairly similar P/E to the market. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh on the share price eventually.

The Bottom Line On Yenher Holdings Berhad's P/E

Yenher Holdings Berhad appears to be back in favour with a solid price jump getting its P/E back in line with most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Yenher Holdings Berhad revealed its shrinking earnings over the medium-term aren't impacting its P/E as much as we would have predicted, given the market is set to grow. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless the recent medium-term conditions improve, it's challenging to accept these prices as being reasonable.

It is also worth noting that we have found 3 warning signs for Yenher Holdings Berhad (1 is significant!) that you need to take into consideration.

If you're unsure about the strength of Yenher Holdings Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:YENHER

Yenher Holdings Berhad

An investment holding company, engages in manufacturing, suppling, and marketing of animal health and nutrition products for livestock and companion animals in Malaysia and internationally.

Flawless balance sheet with moderate growth potential.