Sime Darby Plantation Berhad (KLSE:SIMEPLT) Is Paying Out A Larger Dividend Than Last Year

The board of Sime Darby Plantation Berhad (KLSE:SIMEPLT) has announced that it will be paying its dividend of MYR0.0605 on the 20th of May, an increased payment from last year's comparable dividend. This takes the annual payment to 2.1% of the current stock price, which unfortunately is below what the industry is paying.

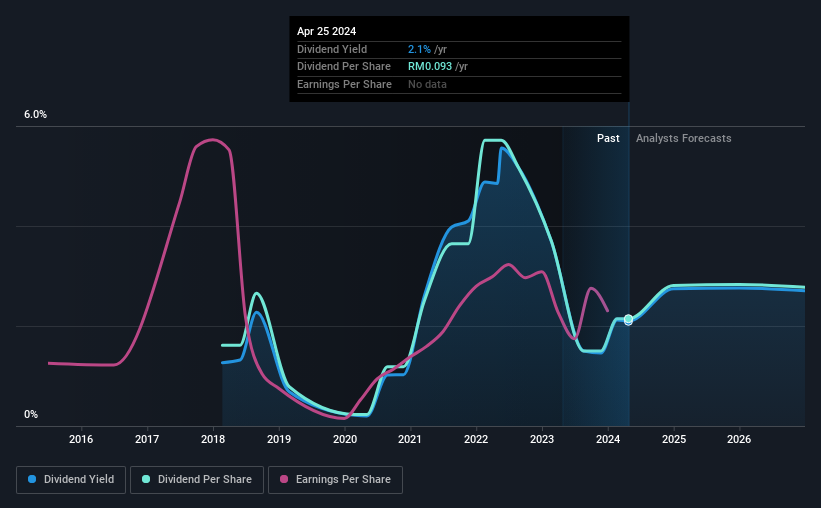

Check out our latest analysis for Sime Darby Plantation Berhad

Sime Darby Plantation Berhad's Earnings Easily Cover The Distributions

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. However, prior to this announcement, Sime Darby Plantation Berhad's dividend was comfortably covered by both cash flow and earnings. As a result, a large proportion of what it earned was being reinvested back into the business.

Over the next year, EPS is forecast to fall by 18.3%. Assuming the dividend continues along recent trends, we believe the payout ratio could be 72%, which we are pretty comfortable with and we think is feasible on an earnings basis.

Sime Darby Plantation Berhad's Dividend Has Lacked Consistency

It's comforting to see that Sime Darby Plantation Berhad has been paying a dividend for a number of years now, however it has been cut at least once in that time. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2018, the dividend has gone from MYR0.07 total annually to MYR0.093. This implies that the company grew its distributions at a yearly rate of about 4.8% over that duration. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Sime Darby Plantation Berhad has impressed us by growing EPS at 25% per year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

We Really Like Sime Darby Plantation Berhad's Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. The company is generating plenty of cash, and the earnings also quite easily cover the distributions. We should point out that the earnings are expected to fall over the next 12 months, which won't be a problem if this doesn't become a trend, but could cause some turbulence in the next year. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, Sime Darby Plantation Berhad has 2 warning signs (and 1 which is potentially serious) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SDG

SD Guthrie Berhad

An investment holding company, operates as an integrated plantations company in Malaysia and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Community Narratives