Is Pinehill Pacific Berhad (KLSE:PINEPAC) A Future Multi-bagger?

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So on that note, Pinehill Pacific Berhad (KLSE:PINEPAC) looks quite promising in regards to its trends of return on capital.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Pinehill Pacific Berhad, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

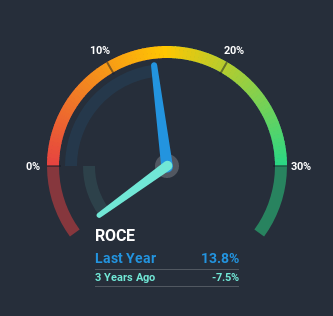

0.14 = RM28m ÷ (RM210m - RM7.3m) (Based on the trailing twelve months to September 2020).

Therefore, Pinehill Pacific Berhad has an ROCE of 14%. In absolute terms, that's a satisfactory return, but compared to the Food industry average of 6.8% it's much better.

View our latest analysis for Pinehill Pacific Berhad

Historical performance is a great place to start when researching a stock so above you can see the gauge for Pinehill Pacific Berhad's ROCE against it's prior returns. If you're interested in investigating Pinehill Pacific Berhad's past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Pinehill Pacific Berhad's ROCE Trending?

Like most people, we're pleased that Pinehill Pacific Berhad is now generating some pretax earnings. The company was generating losses five years ago, but now it's turned around, earning 14% which is no doubt a relief for some early shareholders. At first glance, it seems the business is getting more proficient at generating returns, because over the same period, the amount of capital employed has reduced by 35%. The reduction could indicate that the company is selling some assets, and considering returns are up, they appear to be selling the right ones.

On a related note, the company's ratio of current liabilities to total assets has decreased to 3.5%, which basically reduces it's funding from the likes of short-term creditors or suppliers. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.The Bottom Line On Pinehill Pacific Berhad's ROCE

In summary, it's great to see that Pinehill Pacific Berhad has been able to turn things around and earn higher returns on lower amounts of capital. Since the stock has returned a solid 87% to shareholders over the last five years, it's fair to say investors are beginning to recognize these changes. In light of that, we think it's worth looking further into this stock because if Pinehill Pacific Berhad can keep these trends up, it could have a bright future ahead.

One more thing: We've identified 3 warning signs with Pinehill Pacific Berhad (at least 1 which is significant) , and understanding them would certainly be useful.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

When trading Pinehill Pacific Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:PINEPAC

Pinehill Pacific Berhad

An investment holding company, engages in the oil palm cultivation and processing business in Indonesia.

Flawless balance sheet slight.

Market Insights

Community Narratives