Advertisement

With EPS Growth And More, Lay Hong Berhad (KLSE:LAYHONG) Makes An Interesting Case

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Lay Hong Berhad (KLSE:LAYHONG). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Lay Hong Berhad with the means to add long-term value to shareholders.

Check out our latest analysis for Lay Hong Berhad

How Fast Is Lay Hong Berhad Growing Its Earnings Per Share?

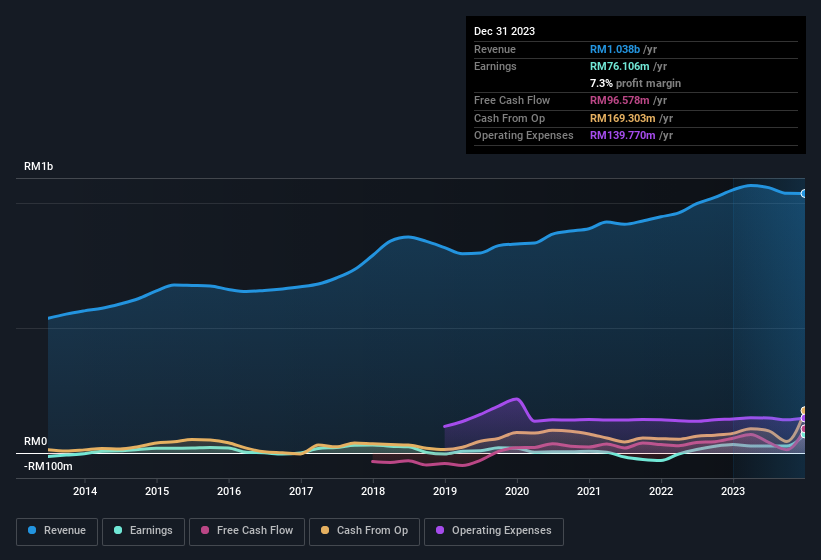

In the last three years Lay Hong Berhad's earnings per share took off; so much so that it's a bit disingenuous to use these figures to try and deduce long term estimates. As a result, we'll zoom in on growth over the last year, instead. Outstandingly, Lay Hong Berhad's EPS shot from RM0.046 to RM0.10, over the last year. It's not often a company can achieve year-on-year growth of 123%.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While revenue is looking a bit flat, the good news is EBIT margins improved by 4.8 percentage points to 11%, in the last twelve months. That's a real positive.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

Lay Hong Berhad isn't a huge company, given its market capitalisation of RM305m. That makes it extra important to check on its balance sheet strength.

Are Lay Hong Berhad Insiders Aligned With All Shareholders?

It should give investors a sense of security owning shares in a company if insiders also own shares, creating a close alignment their interests. Lay Hong Berhad followers will find comfort in knowing that insiders have a significant amount of capital that aligns their best interests with the wider shareholder group. To be specific, they have RM57m worth of shares. This considerable investment should help drive long-term value in the business. As a percentage, this totals to 19% of the shares on issue for the business, an appreciable amount considering the market cap.

Is Lay Hong Berhad Worth Keeping An Eye On?

Lay Hong Berhad's earnings have taken off in quite an impressive fashion. That sort of growth is nothing short of eye-catching, and the large investment held by insiders should certainly brighten the view of the company. At times fast EPS growth is a sign the business has reached an inflection point, so there's a potential opportunity to be had here. Based on the sum of its parts, we definitely think its worth watching Lay Hong Berhad very closely. However, before you get too excited we've discovered 1 warning sign for Lay Hong Berhad that you should be aware of.

Although Lay Hong Berhad certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with insider buying, then check out this handpicked selection of Malaysian companies that not only boast of strong growth but have also seen recent insider buying..

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:LAYHONG

Lay Hong Berhad

An investment holding company, engages in the integrated livestock farming in Malaysia.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|59.6% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.8% undervalued

ZW

Community Contributor