I Ran A Stock Scan For Earnings Growth And Kretam Holdings Berhad (KLSE:KRETAM) Passed With Ease

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

If, on the other hand, you like companies that have revenue, and even earn profits, then you may well be interested in Kretam Holdings Berhad (KLSE:KRETAM). While that doesn't make the shares worth buying at any price, you can't deny that successful capitalism requires profit, eventually. Loss-making companies are always racing against time to reach financial sustainability, but time is often a friend of the profitable company, especially if it is growing.

Check out our latest analysis for Kretam Holdings Berhad

How Fast Is Kretam Holdings Berhad Growing Its Earnings Per Share?

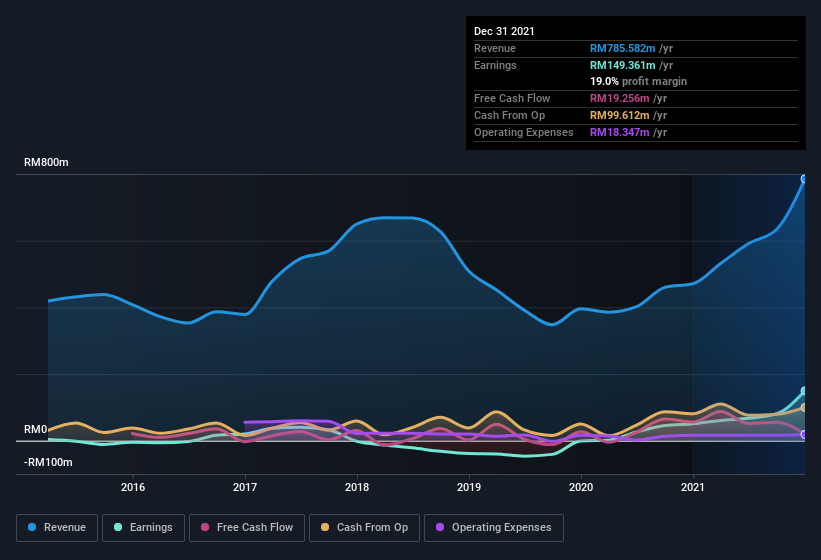

Over the last three years, Kretam Holdings Berhad has grown earnings per share (EPS) like young bamboo after rain; fast, and from a low base. So I don't think the percent growth rate is particularly meaningful. Thus, it makes sense to focus on more recent growth rates, instead. Like a firecracker arcing through the night sky, Kretam Holdings Berhad's EPS shot from RM0.022 to RM0.064, over the last year. You don't see 197% year-on-year growth like that, very often. That could be a sign that the business has reached a true inflection point.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. The good news is that Kretam Holdings Berhad is growing revenues, and EBIT margins improved by 9.0 percentage points to 20%, over the last year. That's great to see, on both counts.

In the chart below, you can see how the company has grown earnings, and revenue, over time. Click on the chart to see the exact numbers.

While it's always good to see growing profits, you should always remember that a weak balance sheet could come back to bite. So check Kretam Holdings Berhad's balance sheet strength, before getting too excited.

Are Kretam Holdings Berhad Insiders Aligned With All Shareholders?

Many consider high insider ownership to be a strong sign of alignment between the leaders of a company and the ordinary shareholders. So we're pleased to report that Kretam Holdings Berhad insiders own a meaningful share of the business. Indeed, with a collective holding of 53%, company insiders are in control and have plenty of capital behind the venture. This makes me think they will be incentivised to plan for the long term - something I like to see. In terms of absolute value, insiders have RM737m invested in the business, using the current share price. That should be more than enough to keep them focussed on creating shareholder value!

Should You Add Kretam Holdings Berhad To Your Watchlist?

Kretam Holdings Berhad's earnings have taken off like any random crypto-currency did, back in 2017. That EPS growth certainly has my attention, and the large insider ownership only serves to further stoke my interest. The hope is, of course, that the strong growth marks a fundamental improvement in the business economics. So yes, on this short analysis I do think it's worth considering Kretam Holdings Berhad for a spot on your watchlist. You still need to take note of risks, for example - Kretam Holdings Berhad has 2 warning signs we think you should be aware of.

Although Kretam Holdings Berhad certainly looks good to me, I would like it more if insiders were buying up shares. If you like to see insider buying, too, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Kretam Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KRETAM

Kretam Holdings Berhad

An investment holding company, engages in the operation of oil palm plantations in Malaysia, Africa, Germany, India, Italy, Malaysia, and the Netherlands.

Flawless balance sheet and good value.

Market Insights

Community Narratives