Advertisement

Kuala Lumpur Kepong Berhad's (KLSE:KLK) CEO Compensation Is Looking A Bit Stretched At The Moment

Under the guidance of CEO Seri Oi Hian Lee, Kuala Lumpur Kepong Berhad (KLSE:KLK) has performed reasonably well recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 23 February 2023. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

See our latest analysis for Kuala Lumpur Kepong Berhad

Comparing Kuala Lumpur Kepong Berhad's CEO Compensation With The Industry

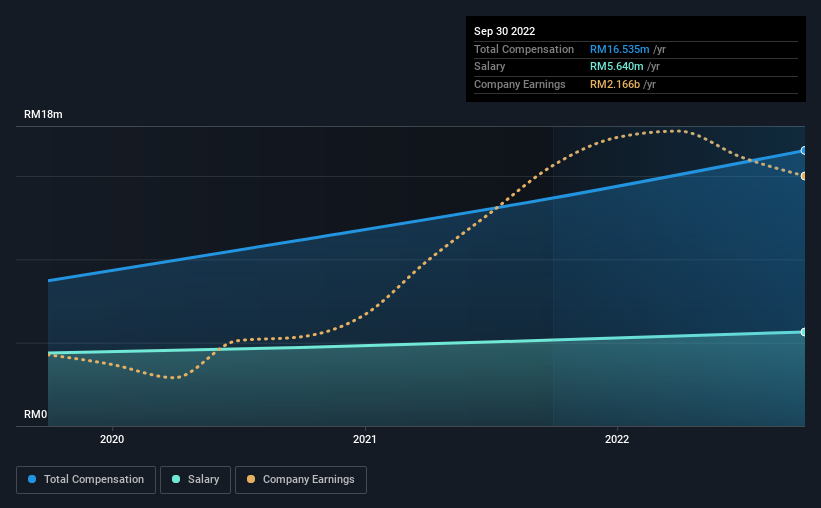

At the time of writing, our data shows that Kuala Lumpur Kepong Berhad has a market capitalization of RM24b, and reported total annual CEO compensation of RM17m for the year to September 2022. That's a notable increase of 21% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at RM5.6m.

In comparison with other companies in the Malaysian Food industry with market capitalizations ranging from RM18b to RM53b, the reported median CEO total compensation was RM3.5m. Hence, we can conclude that Seri Oi Hian Lee is remunerated higher than the industry median. What's more, Seri Oi Hian Lee holds RM3.3m worth of shares in the company in their own name.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | RM5.6m | RM5.2m | 34% |

| Other | RM11m | RM8.5m | 66% |

| Total Compensation | RM17m | RM14m | 100% |

On an industry level, roughly 75% of total compensation represents salary and 25% is other remuneration. Kuala Lumpur Kepong Berhad pays a modest slice of remuneration through salary, as compared to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Kuala Lumpur Kepong Berhad's Growth

Kuala Lumpur Kepong Berhad has seen its earnings per share (EPS) increase by 51% a year over the past three years. In the last year, its revenue is up 36%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The combination of strong revenue growth with medium-term EPS improvement certainly points to the kind of growth we like to see. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Kuala Lumpur Kepong Berhad Been A Good Investment?

Kuala Lumpur Kepong Berhad has generated a total shareholder return of 7.9% over three years, so most shareholders wouldn't be too disappointed. Although, there's always room to improve. In light of that, investors might probably want to see an improvement on their returns before they feel generous about increasing the CEO remuneration.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We did our research and identified 3 warning signs (and 1 which is significant) in Kuala Lumpur Kepong Berhad we think you should know about.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Kuala Lumpur Kepong Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KLK

Kuala Lumpur Kepong Berhad

Engages in the plantation, manufacturing, and property development businesses.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor