Advertisement

- Malaysia

- /

- Energy Services

- /

- KLSE:PERDANA

These 4 Measures Indicate That Perdana Petroleum Berhad (KLSE:PERDANA) Is Using Debt Safely

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Perdana Petroleum Berhad (KLSE:PERDANA) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Perdana Petroleum Berhad

How Much Debt Does Perdana Petroleum Berhad Carry?

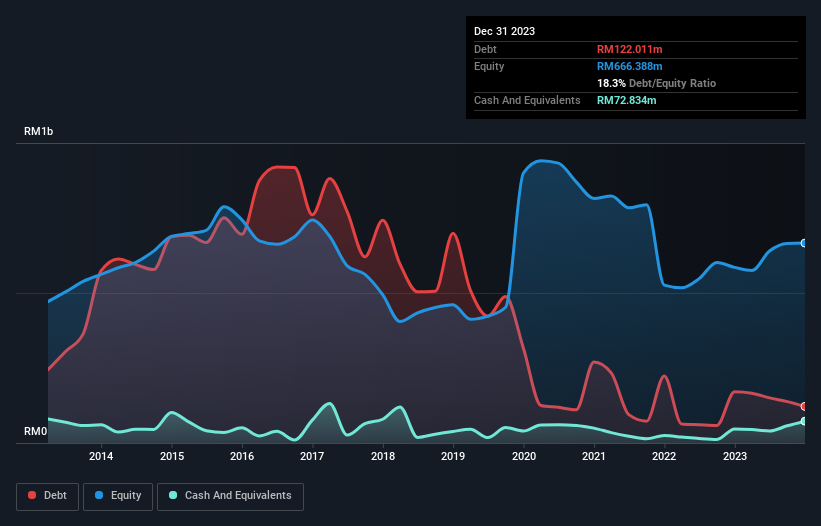

You can click the graphic below for the historical numbers, but it shows that Perdana Petroleum Berhad had RM122.0m of debt in December 2023, down from RM170.8m, one year before. On the flip side, it has RM72.8m in cash leading to net debt of about RM49.2m.

A Look At Perdana Petroleum Berhad's Liabilities

The latest balance sheet data shows that Perdana Petroleum Berhad had liabilities of RM123.9m due within a year, and liabilities of RM117.6m falling due after that. Offsetting this, it had RM72.8m in cash and RM127.7m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM40.9m.

Of course, Perdana Petroleum Berhad has a market capitalization of RM677.3m, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Perdana Petroleum Berhad has net debt of just 0.38 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 9.6 times, which is more than adequate. Even more impressive was the fact that Perdana Petroleum Berhad grew its EBIT by 731% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But it is Perdana Petroleum Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last two years, Perdana Petroleum Berhad actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Happily, Perdana Petroleum Berhad's impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And that's just the beginning of the good news since its EBIT growth rate is also very heartening. We think Perdana Petroleum Berhad is no more beholden to its lenders, than the birds are to birdwatchers. For investing nerds like us its balance sheet is almost charming. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Perdana Petroleum Berhad's earnings per share history for free.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:PERDANA

Perdana Petroleum Berhad

An investment holding company, provides offshore marine support services for the upstream oil and gas industry in Malaysia.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor