Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that KUB Malaysia Berhad (KLSE:KUB) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for KUB Malaysia Berhad

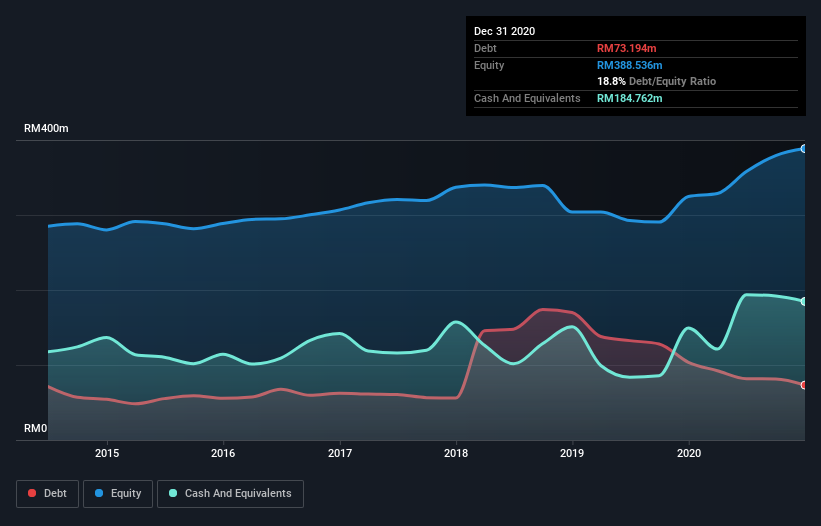

How Much Debt Does KUB Malaysia Berhad Carry?

As you can see below, KUB Malaysia Berhad had RM73.2m of debt at December 2020, down from RM103.6m a year prior. However, its balance sheet shows it holds RM184.8m in cash, so it actually has RM111.6m net cash.

How Strong Is KUB Malaysia Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that KUB Malaysia Berhad had liabilities of RM77.7m due within 12 months and liabilities of RM103.8m due beyond that. Offsetting these obligations, it had cash of RM184.8m as well as receivables valued at RM58.4m due within 12 months. So it can boast RM61.7m more liquid assets than total liabilities.

It's good to see that KUB Malaysia Berhad has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Simply put, the fact that KUB Malaysia Berhad has more cash than debt is arguably a good indication that it can manage its debt safely.

Better yet, KUB Malaysia Berhad grew its EBIT by 200% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since KUB Malaysia Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. KUB Malaysia Berhad may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last two years, KUB Malaysia Berhad basically broke even on a free cash flow basis. While many companies do operate at break-even, we prefer see substantial free cash flow, especially if a it already has dead.

Summing up

While it is always sensible to investigate a company's debt, in this case KUB Malaysia Berhad has RM111.6m in net cash and a decent-looking balance sheet. And it impressed us with its EBIT growth of 200% over the last year. So is KUB Malaysia Berhad's debt a risk? It doesn't seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for KUB Malaysia Berhad (1 doesn't sit too well with us) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if KUB Malaysia Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:KUB

KUB Malaysia Berhad

An investment holding company, engages in the business of importing, storing, bottling, marketing, trading, and distributing liquefied petroleum gas (LPG) for household and industrial use under the Solar Gas brand name in Malaysia.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|36.8% undervalued

TR

Community Contributor