Advertisement

- Malaysia

- /

- Energy Services

- /

- KLSE:ARMADA

Increases to CEO Compensation Might Be Put On Hold For Now at Bumi Armada Berhad (KLSE:ARMADA)

Key Insights

- Bumi Armada Berhad to hold its Annual General Meeting on 30th of May

- CEO Gary Christenson's total compensation includes salary of RM3.06m

- The total compensation is 1,186% higher than the average for the industry

- Over the past three years, Bumi Armada Berhad's EPS grew by 47% and over the past three years, the total shareholder return was 31%

CEO Gary Christenson has done a decent job of delivering relatively good performance at Bumi Armada Berhad (KLSE:ARMADA) recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 30th of May. However, some shareholders will still be cautious of paying the CEO excessively.

Check out our latest analysis for Bumi Armada Berhad

How Does Total Compensation For Gary Christenson Compare With Other Companies In The Industry?

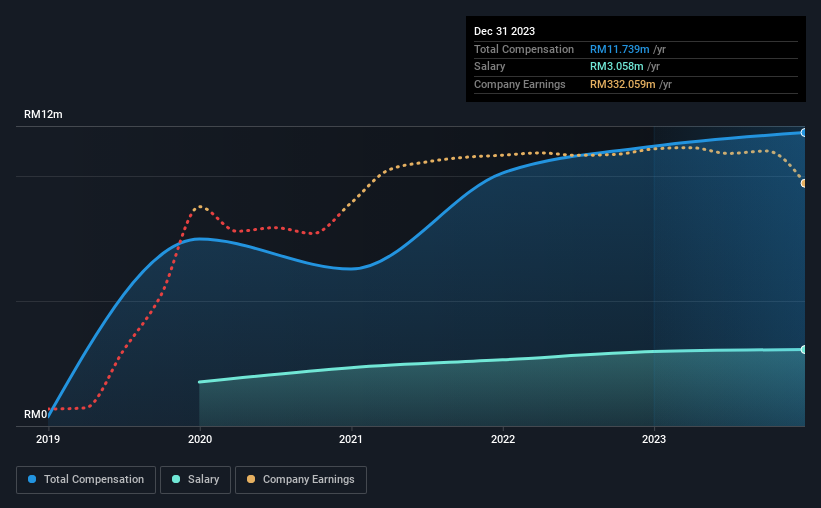

At the time of writing, our data shows that Bumi Armada Berhad has a market capitalization of RM3.4b, and reported total annual CEO compensation of RM12m for the year to December 2023. That's just a smallish increase of 4.9% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at RM3.1m.

In comparison with other companies in the Malaysian Energy Services industry with market capitalizations ranging from RM1.9b to RM7.5b, the reported median CEO total compensation was RM913k. This suggests that Gary Christenson is paid more than the median for the industry. Furthermore, Gary Christenson directly owns RM23m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | RM3.1m | RM3.0m | 26% |

| Other | RM8.7m | RM8.2m | 74% |

| Total Compensation | RM12m | RM11m | 100% |

On an industry level, roughly 59% of total compensation represents salary and 41% is other remuneration. It's interesting to note that Bumi Armada Berhad allocates a smaller portion of compensation to salary in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Bumi Armada Berhad's Growth Numbers

Bumi Armada Berhad has seen its earnings per share (EPS) increase by 47% a year over the past three years. In the last year, its revenue is down 11%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Bumi Armada Berhad Been A Good Investment?

Bumi Armada Berhad has served shareholders reasonably well, with a total return of 31% over three years. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 3 warning signs for Bumi Armada Berhad that you should be aware of before investing.

Important note: Bumi Armada Berhad is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Bumi Armada Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:ARMADA

Bumi Armada Berhad

An investment holding company, engages in providing marine transportation, floating production storage offloading (FPSO) operations, and engineering and maintenance services to offshore oil and gas companies.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor