Advertisement

- Malaysia

- /

- Consumer Finance

- /

- KLSE:WELLCHIP

What You Need To Know About The Well Chip Group Berhad (KLSE:WELLCHIP) Analyst Downgrade Today

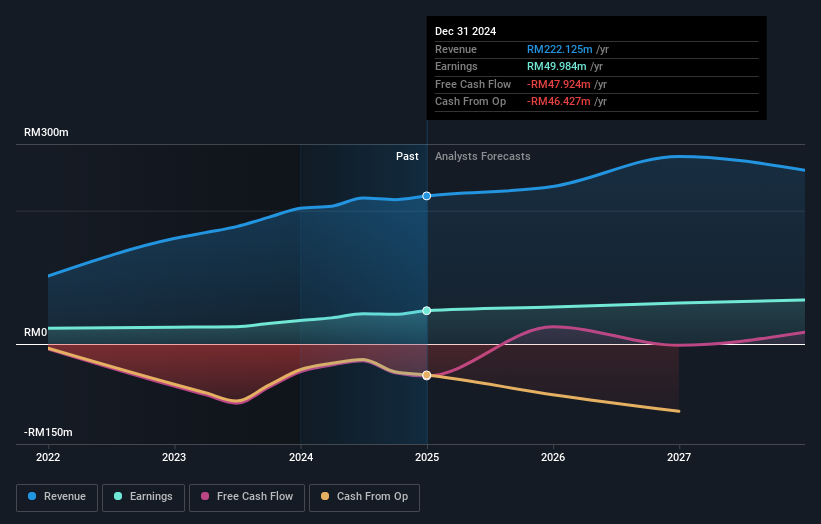

Today is shaping up negative for Well Chip Group Berhad (KLSE:WELLCHIP) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic.

Following the downgrade, the latest consensus from Well Chip Group Berhad's twin analysts is for revenues of RM236m in 2025, which would reflect a modest 6.3% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to swell 12% to RM0.093. Before this latest update, the analysts had been forecasting revenues of RM264m and earnings per share (EPS) of RM0.10 in 2025. It looks like analyst sentiment has fallen somewhat in this update, with a substantial drop in revenue estimates and a small dip in earnings per share numbers as well.

Check out our latest analysis for Well Chip Group Berhad

Analysts made no major changes to their price target of RM1.76, suggesting the downgrades are not expected to have a long-term impact on Well Chip Group Berhad's valuation.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that Well Chip Group Berhad's revenue growth is expected to slow, with the forecast 6.3% annualised growth rate until the end of 2025 being well below the historical 22% p.a. growth over the last three years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 20% annually. Factoring in the forecast slowdown in growth, it seems obvious that Well Chip Group Berhad is also expected to grow slower than other industry participants.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Well Chip Group Berhad. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Well Chip Group Berhad's revenues are expected to grow slower than the wider market. Given the stark change in sentiment, we'd understand if investors became more cautious on Well Chip Group Berhad after today.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Well Chip Group Berhad going out as far as 2027, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Well Chip Group Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:WELLCHIP

Well Chip Group Berhad

An investment holding company, engages in the provision of pawnbroking services, and retail and trading of jewelry and gold in Malaysia.

Proven track record with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|26.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|21.3% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|61.2% undervalued

ME

Community Contributor