- Malaysia

- /

- Hospitality

- /

- KLSE:EXSIMHB

Pan Malaysia Holdings Berhad (KLSE:PMHLDG) Is Making Moderate Use Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Pan Malaysia Holdings Berhad (KLSE:PMHLDG) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Pan Malaysia Holdings Berhad

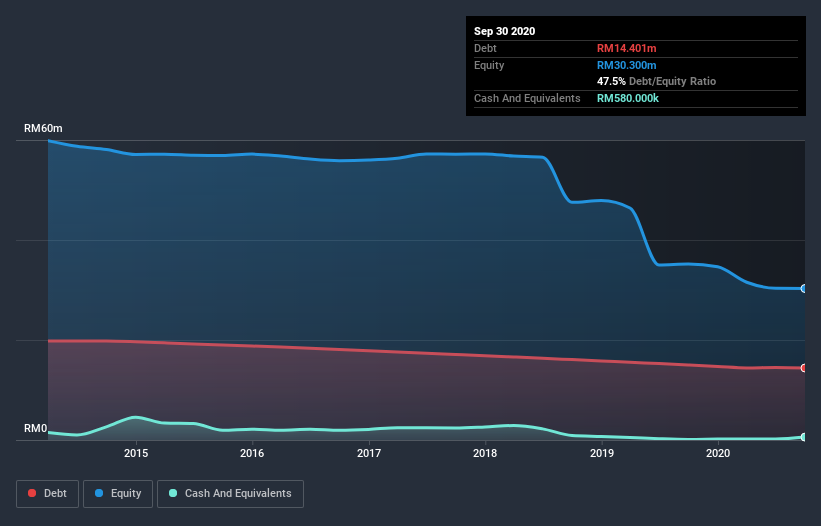

What Is Pan Malaysia Holdings Berhad's Debt?

The chart below, which you can click on for greater detail, shows that Pan Malaysia Holdings Berhad had RM14.4m in debt in September 2020; about the same as the year before. However, it also had RM580.0k in cash, and so its net debt is RM13.8m.

How Healthy Is Pan Malaysia Holdings Berhad's Balance Sheet?

We can see from the most recent balance sheet that Pan Malaysia Holdings Berhad had liabilities of RM7.97m falling due within a year, and liabilities of RM13.8m due beyond that. On the other hand, it had cash of RM580.0k and RM1.05m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by RM20.1m.

While this might seem like a lot, it is not so bad since Pan Malaysia Holdings Berhad has a market capitalization of RM97.5m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Pan Malaysia Holdings Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Pan Malaysia Holdings Berhad had a loss before interest and tax, and actually shrunk its revenue by 30%, to RM5.8m. To be frank that doesn't bode well.

Caveat Emptor

While Pan Malaysia Holdings Berhad's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. To be specific the EBIT loss came in at RM3.4m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. We would feel better if it turned its trailing twelve month loss of RM4.0m into a profit. So we do think this stock is quite risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Consider for instance, the ever-present spectre of investment risk. We've identified 4 warning signs with Pan Malaysia Holdings Berhad (at least 1 which is significant) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Pan Malaysia Holdings Berhad, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Exsim Hospitality Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:EXSIMHB

Exsim Hospitality Berhad

An investment holding company, engages in the hotel business in Malaysia.

Adequate balance sheet very low.

Market Insights

Community Narratives