Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Pan Malaysia Holdings Berhad (KLSE:PMHLDG) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Pan Malaysia Holdings Berhad

What Is Pan Malaysia Holdings Berhad's Net Debt?

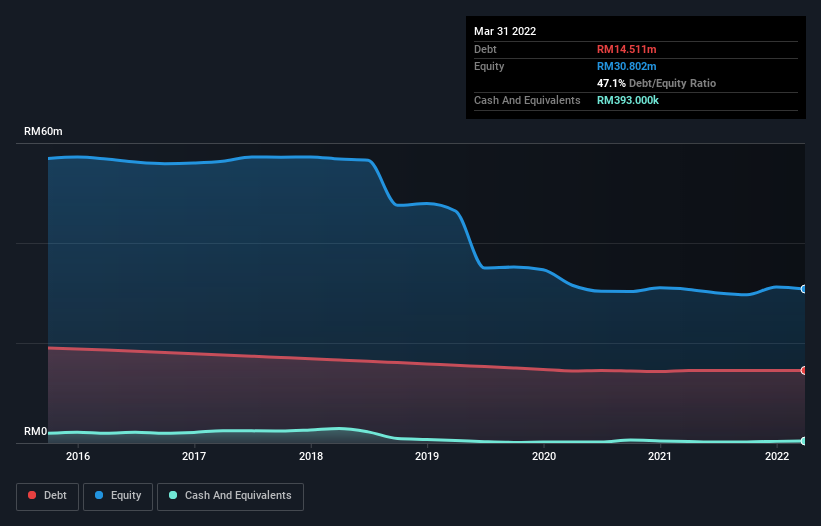

As you can see below, Pan Malaysia Holdings Berhad had RM14.5m of debt, at March 2022, which is about the same as the year before. You can click the chart for greater detail. However, it also had RM393.0k in cash, and so its net debt is RM14.1m.

A Look At Pan Malaysia Holdings Berhad's Liabilities

Zooming in on the latest balance sheet data, we can see that Pan Malaysia Holdings Berhad had liabilities of RM6.56m due within 12 months and liabilities of RM14.8m due beyond that. On the other hand, it had cash of RM393.0k and RM32.7m worth of receivables due within a year. So it can boast RM11.7m more liquid assets than total liabilities.

This surplus suggests that Pan Malaysia Holdings Berhad is using debt in a way that is appears to be both safe and conservative. Due to its strong net asset position, it is not likely to face issues with its lenders.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 0.93 times and a disturbingly high net debt to EBITDA ratio of 8.0 hit our confidence in Pan Malaysia Holdings Berhad like a one-two punch to the gut. The debt burden here is substantial. However, the silver lining was that Pan Malaysia Holdings Berhad achieved a positive EBIT of RM752k in the last twelve months, an improvement on the prior year's loss. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Pan Malaysia Holdings Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. In the last year, Pan Malaysia Holdings Berhad's free cash flow amounted to 22% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Both Pan Malaysia Holdings Berhad's interest cover and its net debt to EBITDA were discouraging. At least its level of total liabilities gives us reason to be optimistic. We think that Pan Malaysia Holdings Berhad's debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for Pan Malaysia Holdings Berhad (2 are significant!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Exsim Hospitality Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:EXSIMHB

Exsim Hospitality Berhad

An investment holding company, engages in the hotel business in Malaysia.

Adequate balance sheet very low.

Market Insights

Community Narratives