Advertisement

- Malaysia

- /

- Hospitality

- /

- KLSE:ICONIC

We're Not Counting On Iconic Worldwide Berhad (KLSE:ICONIC) To Sustain Its Statutory Profitability

Broadly speaking, profitable businesses are less risky than unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. This article will consider whether Iconic Worldwide Berhad's (KLSE:ICONIC) statutory profits are a good guide to its underlying earnings.

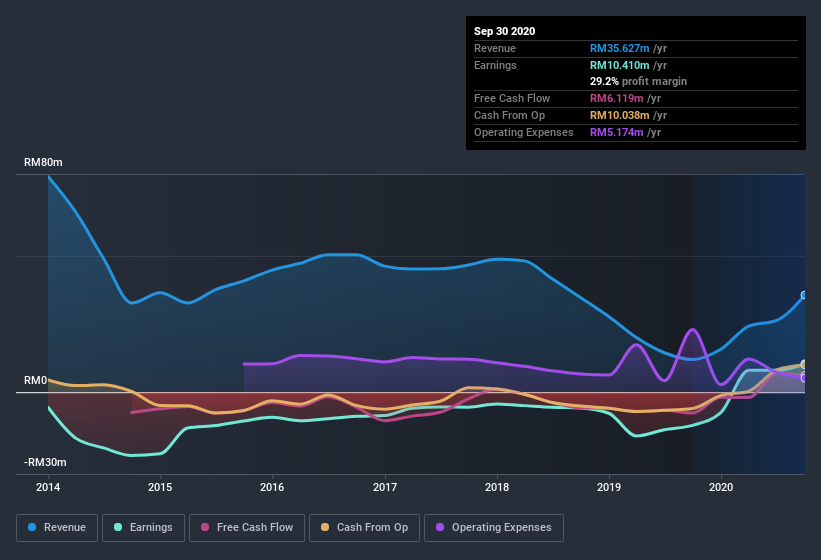

It's good to see that over the last twelve months Iconic Worldwide Berhad made a profit of RM10.4m on revenue of RM35.6m. Even though revenue is down over the last three years, you can see in the chart below that the company has moved from loss-making to profitable.

See our latest analysis for Iconic Worldwide Berhad

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. In this article we will consider how Iconic Worldwide Berhad's decision to issue new shares in the company has impacted returns to shareholders. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Iconic Worldwide Berhad.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, Iconic Worldwide Berhad increased the number of shares on issue by 30% over the last twelve months by issuing new shares. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of Iconic Worldwide Berhad's EPS by clicking here.

A Look At The Impact Of Iconic Worldwide Berhad's Dilution on Its Earnings Per Share (EPS).

Iconic Worldwide Berhad was losing money three years ago. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

If Iconic Worldwide Berhad's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On Iconic Worldwide Berhad's Profit Performance

Over the last year Iconic Worldwide Berhad issued new shares and so, there's a noteworthy divergence between EPS and net income growth. Therefore, it seems possible to us that Iconic Worldwide Berhad's true underlying earnings power is actually less than its statutory profit. The good news is that it earned a profit in the last twelve months, despite its previous loss. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. At Simply Wall St, we found 2 warning signs for Iconic Worldwide Berhad and we think they deserve your attention.

Today we've zoomed in on a single data point to better understand the nature of Iconic Worldwide Berhad's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you’re looking to trade Iconic Worldwide Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:ICONIC

Iconic Worldwide Berhad

An investment holding company, engages in tourism and property businesses in Malaysia, Turkey, Australia, Hong Kong, Thailand, Philippines, and the Middle East.

Low with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor