- Malaysia

- /

- Food and Staples Retail

- /

- KLSE:SEM

Don't Race Out To Buy 7-Eleven Malaysia Holdings Berhad (KLSE:SEM) Just Because It's Going Ex-Dividend

Readers hoping to buy 7-Eleven Malaysia Holdings Berhad (KLSE:SEM) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. This means that investors who purchase 7-Eleven Malaysia Holdings Berhad's shares on or after the 10th of May will not receive the dividend, which will be paid on the 28th of May.

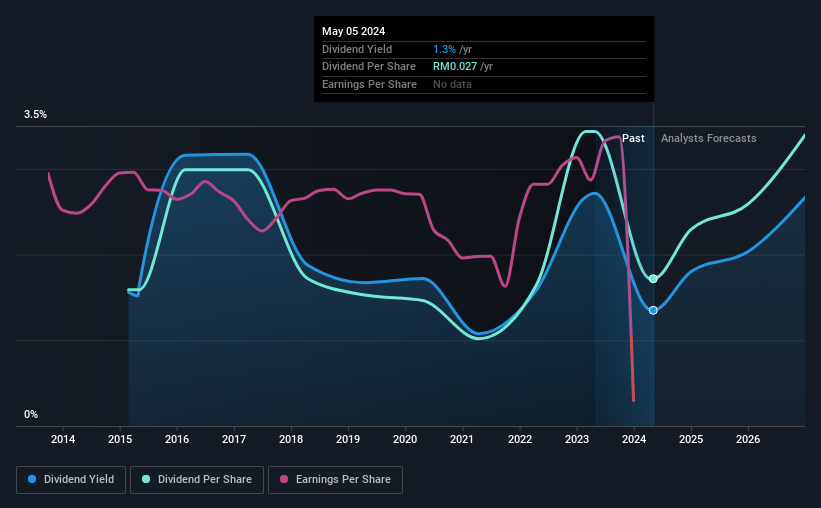

The company's next dividend payment will be RM00.027 per share. Last year, in total, the company distributed RM0.027 to shareholders. Calculating the last year's worth of payments shows that 7-Eleven Malaysia Holdings Berhad has a trailing yield of 1.4% on the current share price of RM02.00. If you buy this business for its dividend, you should have an idea of whether 7-Eleven Malaysia Holdings Berhad's dividend is reliable and sustainable. So we need to investigate whether 7-Eleven Malaysia Holdings Berhad can afford its dividend, and if the dividend could grow.

Check out our latest analysis for 7-Eleven Malaysia Holdings Berhad

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. 7-Eleven Malaysia Holdings Berhad reported a loss after tax last year, which means it's paying a dividend despite being unprofitable. While this might be a one-off event, this is unlikely to be sustainable in the long term. Given that the company reported a loss last year, we now need to see if it generated enough free cash flow to fund the dividend. If cash earnings don't cover the dividend, the company would have to pay dividends out of cash in the bank, or by borrowing money, neither of which is long-term sustainable. It paid out 79% of its free cash flow as dividends, which is within usual limits but will limit the company's ability to lift the dividend if there's no growth.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies that aren't growing their earnings can still be valuable, but it is even more important to assess the sustainability of the dividend if it looks like the company will struggle to grow. If earnings fall far enough, the company could be forced to cut its dividend. 7-Eleven Malaysia Holdings Berhad reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. 7-Eleven Malaysia Holdings Berhad has delivered 0.9% dividend growth per year on average over the past nine years.

We update our analysis on 7-Eleven Malaysia Holdings Berhad every 24 hours, so you can always get the latest insights on its financial health, here.

Final Takeaway

Is 7-Eleven Malaysia Holdings Berhad worth buying for its dividend? First, it's not great to see the company paying a dividend despite being loss-making over the last year. On the plus side, the dividend was covered by free cash flow." It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

Ever wonder what the future holds for 7-Eleven Malaysia Holdings Berhad? See what the three analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SEM

7-Eleven Malaysia Holdings Berhad

An investment holding company, owns, operates, and franchises a chain of convenience stores under the 7-Eleven brand in Malaysia.

High growth potential and good value.

Market Insights

Community Narratives