Advertisement

- Malaysia

- /

- Food and Staples Retail

- /

- KLSE:SEM

7-Eleven Malaysia Holdings Berhad's (KLSE:SEM) Shareholders Will Receive A Bigger Dividend Than Last Year

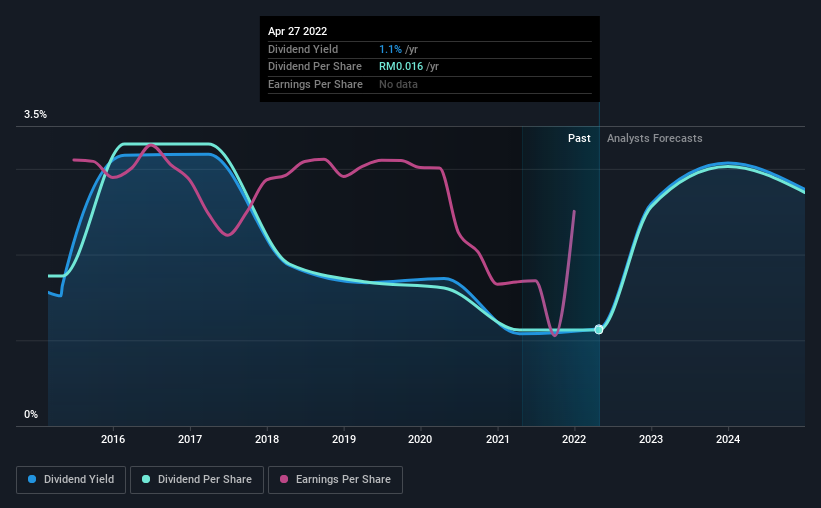

The board of 7-Eleven Malaysia Holdings Berhad (KLSE:SEM) has announced that it will be increasing its dividend by 63% on the 27th of May to RM0.026. The announced payment will take the dividend yield to 1.8%, which is in line with the average for the industry.

View our latest analysis for 7-Eleven Malaysia Holdings Berhad

7-Eleven Malaysia Holdings Berhad's Earnings Easily Cover the Distributions

We like to see a healthy dividend yield, but that is only helpful to us if the payment can continue. Based on the last payment, 7-Eleven Malaysia Holdings Berhad was quite comfortably earning enough to cover the dividend. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

Looking forward, earnings per share is forecast to rise by 59.2% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 43%, which is in the range that makes us comfortable with the sustainability of the dividend.

7-Eleven Malaysia Holdings Berhad's Dividend Has Lacked Consistency

Looking back, 7-Eleven Malaysia Holdings Berhad's dividend hasn't been particularly consistent. This suggests that the dividend might not be the most reliable. The first annual payment during the last 7 years was RM0.025 in 2015, and the most recent fiscal year payment was RM0.016. The dividend has shrunk at around 6.2% a year during that period. A company that decreases its dividend over time generally isn't what we are looking for.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS is growing. 7-Eleven Malaysia Holdings Berhad has seen earnings per share falling at 2.6% per year over the last five years. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think 7-Eleven Malaysia Holdings Berhad's payments are rock solid. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 1 warning sign for 7-Eleven Malaysia Holdings Berhad that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SEM

7-Eleven Malaysia Holdings Berhad

An investment holding company, owns, operates, and franchises a chain of convenience stores under the 7-Eleven brand in Malaysia.

High growth potential and slightly overvalued.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor