Advertisement

- Malaysia

- /

- Consumer Durables

- /

- KLSE:POHUAT

Poh Huat Resources Holdings Berhad Beat Analyst Estimates: See What The Consensus Is Forecasting For This Year

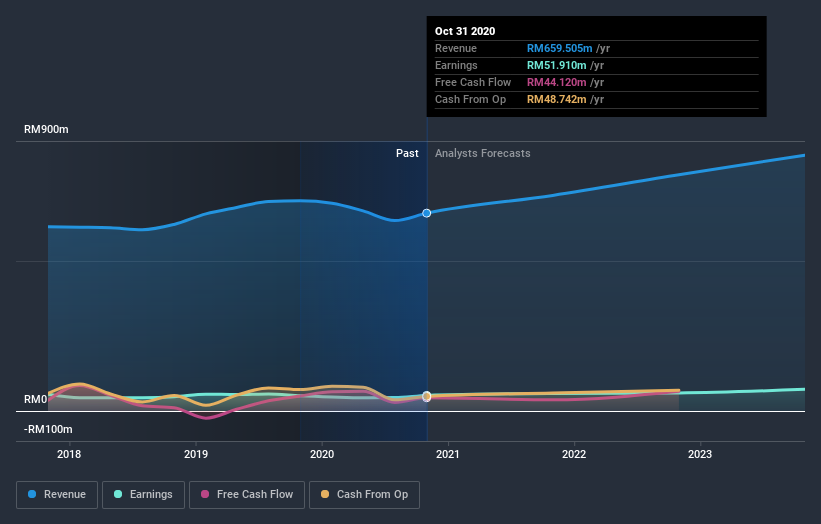

Poh Huat Resources Holdings Berhad (KLSE:POHUAT) just released its latest full-year results and things are looking bullish. The company beat both earnings and revenue forecasts, with revenue of RM660m, some 3.9% above estimates, and statutory earnings per share (EPS) coming in at RM0.22, 34% ahead of expectations. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for Poh Huat Resources Holdings Berhad

After the latest results, the four analysts covering Poh Huat Resources Holdings Berhad are now predicting revenues of RM718.7m in 2021. If met, this would reflect a meaningful 9.0% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to dip 4.8% to RM0.21 in the same period. In the lead-up to this report, the analysts had been modelling revenues of RM721.0m and earnings per share (EPS) of RM0.20 in 2021. The analysts seems to have become more bullish on the business, judging by their new earnings per share estimates.

The consensus price target was unchanged at RM2.02, implying that the improved earnings outlook is not expected to have a long term impact on value creation for shareholders. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Poh Huat Resources Holdings Berhad at RM2.37 per share, while the most bearish prices it at RM1.80. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The analysts are definitely expecting Poh Huat Resources Holdings Berhad's growth to accelerate, with the forecast 9.0% growth ranking favourably alongside historical growth of 7.0% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 8.1% next year. Factoring in the forecast acceleration in revenue, it's pretty clear that Poh Huat Resources Holdings Berhad is expected to grow at about the same rate as the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Poh Huat Resources Holdings Berhad following these results. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. The consensus price target held steady at RM2.02, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Poh Huat Resources Holdings Berhad going out to 2023, and you can see them free on our platform here..

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Poh Huat Resources Holdings Berhad , and understanding these should be part of your investment process.

If you’re looking to trade Poh Huat Resources Holdings Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:POHUAT

Poh Huat Resources Holdings Berhad

An investment holding company, manufactures and sells furniture in Malaysia and Vietnam.

Flawless balance sheet with reasonable growth potential and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative