- Malaysia

- /

- Consumer Durables

- /

- KLSE:PENSONI

Here's Why Pensonic Holdings Berhad (KLSE:PENSONI) Can Manage Its Debt Responsibly

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Pensonic Holdings Berhad (KLSE:PENSONI) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Pensonic Holdings Berhad

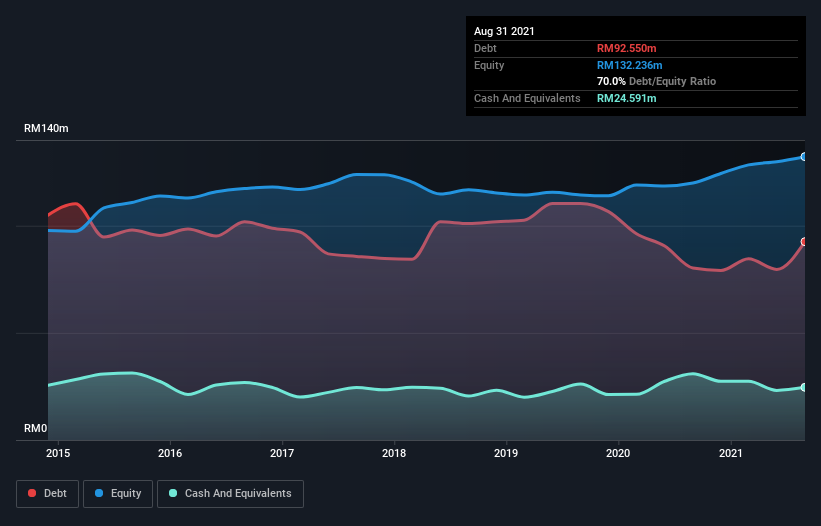

What Is Pensonic Holdings Berhad's Debt?

The image below, which you can click on for greater detail, shows that at August 2021 Pensonic Holdings Berhad had debt of RM92.6m, up from RM80.2m in one year. However, it does have RM24.6m in cash offsetting this, leading to net debt of about RM68.0m.

A Look At Pensonic Holdings Berhad's Liabilities

The latest balance sheet data shows that Pensonic Holdings Berhad had liabilities of RM110.4m due within a year, and liabilities of RM34.0m falling due after that. On the other hand, it had cash of RM24.6m and RM45.8m worth of receivables due within a year. So it has liabilities totalling RM74.1m more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of RM72.0m, we think shareholders really should watch Pensonic Holdings Berhad's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Pensonic Holdings Berhad has a debt to EBITDA ratio of 2.7 and its EBIT covered its interest expense 6.6 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Notably, Pensonic Holdings Berhad's EBIT launched higher than Elon Musk, gaining a whopping 7,983% on last year. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Pensonic Holdings Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Pensonic Holdings Berhad recorded free cash flow worth 62% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

When it comes to the balance sheet, the standout positive for Pensonic Holdings Berhad was the fact that it seems able to grow its EBIT confidently. However, our other observations weren't so heartening. For example, its level of total liabilities makes us a little nervous about its debt. When we consider all the factors mentioned above, we do feel a bit cautious about Pensonic Holdings Berhad's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 4 warning signs with Pensonic Holdings Berhad (at least 1 which makes us a bit uncomfortable) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:PENSONI

Pensonic Holdings Berhad

An investment holding company, manufactures, assembles, and sells electrical and electronic appliances in Malaysia, other Asian countries, the Middle East, and internationally.

Slight with mediocre balance sheet.