- Malaysia

- /

- Consumer Durables

- /

- KLSE:PANAMY

Does Panasonic Manufacturing Malaysia Berhad's (KLSE:PANAMY) Returns On Capital Reflect Well On The Business?

If we're looking to avoid a business that is in decline, what are the trends that can warn us ahead of time? A business that's potentially in decline often shows two trends, a return on capital employed (ROCE) that's declining, and a base of capital employed that's also declining. Trends like this ultimately mean the business is reducing its investments and also earning less on what it has invested. In light of that, from a first glance at Panasonic Manufacturing Malaysia Berhad (KLSE:PANAMY), we've spotted some signs that it could be struggling, so let's investigate.

Return On Capital Employed (ROCE): What is it?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Panasonic Manufacturing Malaysia Berhad is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

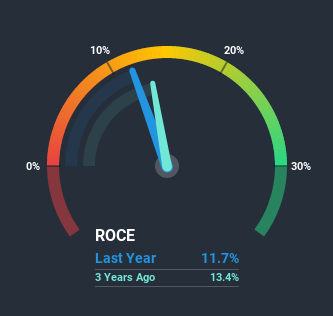

0.12 = RM87m ÷ (RM923m - RM179m) (Based on the trailing twelve months to September 2020).

Thus, Panasonic Manufacturing Malaysia Berhad has an ROCE of 12%. By itself that's a normal return on capital and it's in line with the industry's average returns of 12%.

View our latest analysis for Panasonic Manufacturing Malaysia Berhad

In the above chart we have measured Panasonic Manufacturing Malaysia Berhad's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

What The Trend Of ROCE Can Tell Us

We are a bit worried about the trend of returns on capital at Panasonic Manufacturing Malaysia Berhad. Unfortunately the returns on capital have diminished from the 18% that they were earning five years ago. On top of that, it's worth noting that the amount of capital employed within the business has remained relatively steady. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. So because these trends aren't typically conducive to creating a multi-bagger, we wouldn't hold our breath on Panasonic Manufacturing Malaysia Berhad becoming one if things continue as they have.

Our Take On Panasonic Manufacturing Malaysia Berhad's ROCE

In summary, it's unfortunate that Panasonic Manufacturing Malaysia Berhad is generating lower returns from the same amount of capital. Yet despite these concerning fundamentals, the stock has performed strongly with a 70% return over the last five years, so investors appear very optimistic. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

On a separate note, we've found 2 warning signs for Panasonic Manufacturing Malaysia Berhad you'll probably want to know about.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

When trading Panasonic Manufacturing Malaysia Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:PANAMY

Panasonic Manufacturing Malaysia Berhad

Manufactures and sells electrical home appliances and related components under the Panasonic brand name in Malaysia, Japan, rest of Asia, Europe, the Middle East, and internationally.

Flawless balance sheet with moderate growth potential.