- Malaysia

- /

- Commercial Services

- /

- KLSE:TIENWAH

Tien Wah Press Holdings Berhad (KLSE:TIENWAH) Seems To Use Debt Quite Sensibly

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Tien Wah Press Holdings Berhad (KLSE:TIENWAH) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Tien Wah Press Holdings Berhad

What Is Tien Wah Press Holdings Berhad's Net Debt?

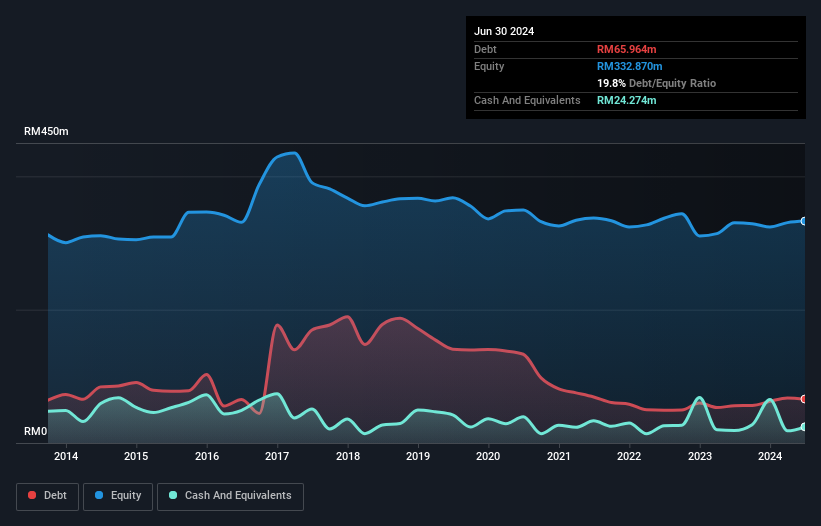

You can click the graphic below for the historical numbers, but it shows that as of June 2024 Tien Wah Press Holdings Berhad had RM66.0m of debt, an increase on RM55.8m, over one year. On the flip side, it has RM24.3m in cash leading to net debt of about RM41.7m.

How Healthy Is Tien Wah Press Holdings Berhad's Balance Sheet?

We can see from the most recent balance sheet that Tien Wah Press Holdings Berhad had liabilities of RM73.5m falling due within a year, and liabilities of RM81.8m due beyond that. Offsetting these obligations, it had cash of RM24.3m as well as receivables valued at RM86.4m due within 12 months. So its liabilities total RM44.6m more than the combination of its cash and short-term receivables.

Tien Wah Press Holdings Berhad has a market capitalization of RM127.4m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Tien Wah Press Holdings Berhad's low debt to EBITDA ratio of 0.86 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 4.7 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Pleasingly, Tien Wah Press Holdings Berhad is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 263% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is Tien Wah Press Holdings Berhad's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Happily for any shareholders, Tien Wah Press Holdings Berhad actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Tien Wah Press Holdings Berhad's conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And the good news does not stop there, as its EBIT growth rate also supports that impression! Looking at the bigger picture, we think Tien Wah Press Holdings Berhad's use of debt seems quite reasonable and we're not concerned about it. While debt does bring risk, when used wisely it can also bring a higher return on equity. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for Tien Wah Press Holdings Berhad that you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Tien Wah Press Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TIENWAH

Tien Wah Press Holdings Berhad

An investment holding company, provides rotogravure and photolithography printing services in Singapore, Indonesia, South Korea, Australasia, Malaysia, Vietnam, Hong Kong, the Middle East, and internationally.

Flawless balance sheet with acceptable track record.

Market Insights

Community Narratives