Advertisement

- Malaysia

- /

- Commercial Services

- /

- KLSE:PICORP

These 4 Measures Indicate That Progressive Impact Corporation Berhad (KLSE:PICORP) Is Using Debt Reasonably Well

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Progressive Impact Corporation Berhad (KLSE:PICORP) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Progressive Impact Corporation Berhad

What Is Progressive Impact Corporation Berhad's Debt?

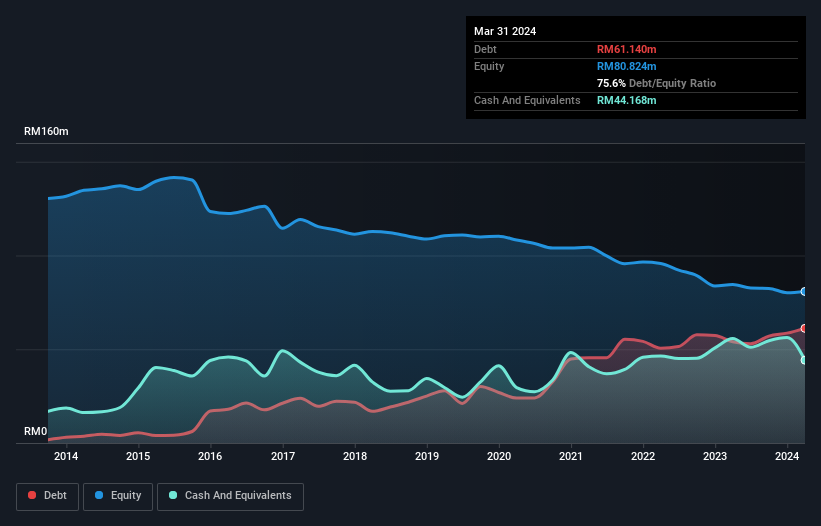

The image below, which you can click on for greater detail, shows that at March 2024 Progressive Impact Corporation Berhad had debt of RM61.1m, up from RM54.0m in one year. On the flip side, it has RM44.2m in cash leading to net debt of about RM17.0m.

How Strong Is Progressive Impact Corporation Berhad's Balance Sheet?

According to the last reported balance sheet, Progressive Impact Corporation Berhad had liabilities of RM90.5m due within 12 months, and liabilities of RM4.84m due beyond 12 months. Offsetting this, it had RM44.2m in cash and RM45.9m in receivables that were due within 12 months. So it has liabilities totalling RM5.26m more than its cash and near-term receivables, combined.

Of course, Progressive Impact Corporation Berhad has a market capitalization of RM45.9m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Progressive Impact Corporation Berhad has a very low debt to EBITDA ratio of 1.1 so it is strange to see weak interest coverage, with last year's EBIT being only 2.0 times the interest expense. So one way or the other, it's clear the debt levels are not trivial. Pleasingly, Progressive Impact Corporation Berhad is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 576% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Progressive Impact Corporation Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Progressive Impact Corporation Berhad actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

The good news is that Progressive Impact Corporation Berhad's demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But the stark truth is that we are concerned by its interest cover. Zooming out, Progressive Impact Corporation Berhad seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Progressive Impact Corporation Berhad (2 shouldn't be ignored!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KLSE:PICORP

Progressive Impact Corporation Berhad

An investment holding company, provides environmental consulting, monitoring equipment and systems integration, environmental data management and laboratory testing services, and wastewater treatment solutions.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor