Advertisement

- Malaysia

- /

- Commercial Services

- /

- KLSE:NGGB

Nextgreen Global Berhad's (KLSE:NGGB) Earnings Aren't As Good As They Appear

After announcing healthy earnings, Nextgreen Global Berhad's (KLSE:NGGB) stock rose over the last week. Despite the strong profit numbers, we believe that there are some deeper issues which investors should look into.

Check out our latest analysis for Nextgreen Global Berhad

A Closer Look At Nextgreen Global Berhad's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

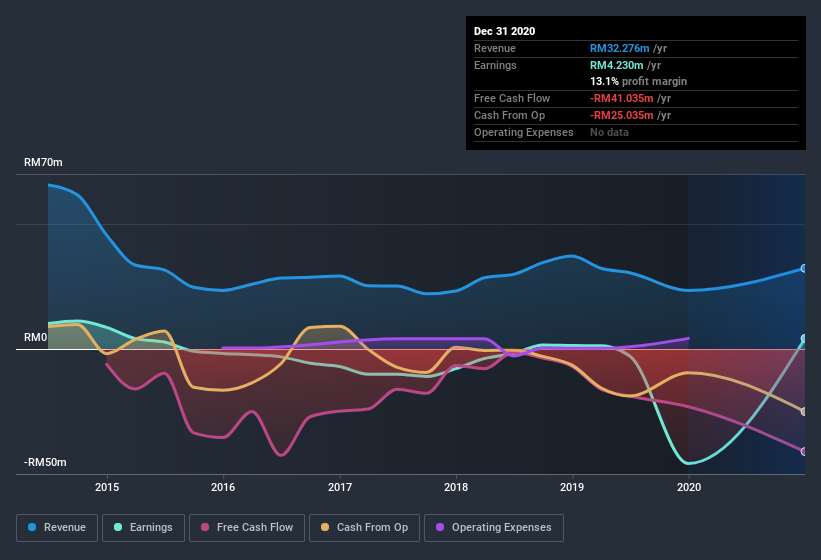

Over the twelve months to December 2020, Nextgreen Global Berhad recorded an accrual ratio of 0.35. We can therefore deduce that its free cash flow fell well short of covering its statutory profit, suggesting we might want to think twice before putting a lot of weight on the latter. Even though it reported a profit of RM4.23m, a look at free cash flow indicates it actually burnt through RM41m in the last year. We also note that Nextgreen Global Berhad's free cash flow was actually negative last year as well, so we could understand if shareholders were bothered by its outflow of RM41m. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings. The good news for shareholders is that Nextgreen Global Berhad's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. Shareholders should look for improved cashflow relative to profit in the current year, if that is indeed the case.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Nextgreen Global Berhad.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. Nextgreen Global Berhad expanded the number of shares on issue by 26% over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of Nextgreen Global Berhad's EPS by clicking here.

How Is Dilution Impacting Nextgreen Global Berhad's Earnings Per Share? (EPS)

Nextgreen Global Berhad was losing money three years ago. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). So you can see that the dilution has had a fairly significant impact on shareholders.

If Nextgreen Global Berhad's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our Take On Nextgreen Global Berhad's Profit Performance

As it turns out, Nextgreen Global Berhad couldn't match its profit with cashflow and its dilution means that shareholders own less of the company than the did before (unless they bought more shares). Considering all this we'd argue Nextgreen Global Berhad's profits probably give an overly generous impression of its sustainable level of profitability. If you want to do dive deeper into Nextgreen Global Berhad, you'd also look into what risks it is currently facing. For example, Nextgreen Global Berhad has 4 warning signs (and 1 which doesn't sit too well with us) we think you should know about.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you’re looking to trade Nextgreen Global Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Nextgreen Global Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:NGGB

Nextgreen Global Berhad

An investment holding company, engages in printing and publishing business in Malaysia, China, France, Singapore, and the United States.

Adequate balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor