Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:WCT

WCT Holdings Berhad (KLSE:WCT) shareholder returns have been notable, earning 92% in 1 year

These days it's easy to simply buy an index fund, and your returns should (roughly) match the market. But one can do better than that by picking better than average stocks (as part of a diversified portfolio). For example, the WCT Holdings Berhad (KLSE:WCT) share price is up 92% in the last 1 year, clearly besting the market return of around 11% (not including dividends). So that should have shareholders smiling. And shareholders have also done well over the long term, with an increase of 91% in the last three years.

Since the stock has added RM148m to its market cap in the past week alone, let's see if underlying performance has been driving long-term returns.

View our latest analysis for WCT Holdings Berhad

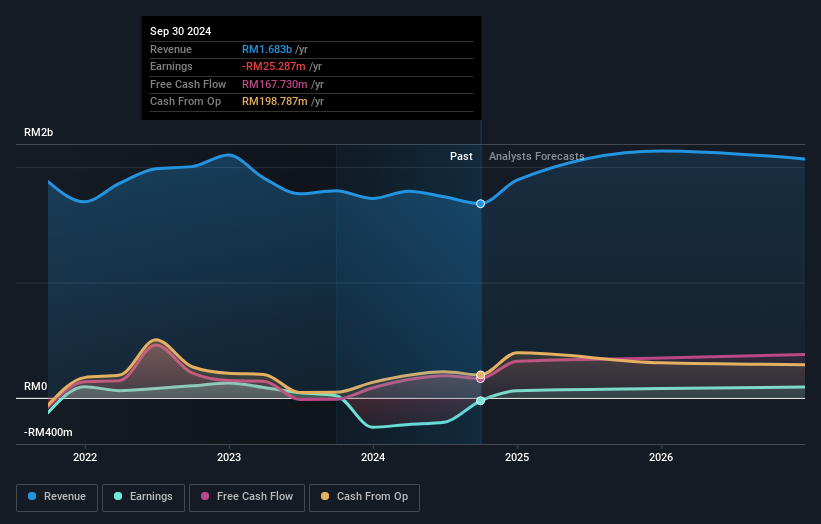

Given that WCT Holdings Berhad didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Shareholders of unprofitable companies usually desire strong revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

WCT Holdings Berhad actually shrunk its revenue over the last year, with a reduction of 6.2%. Despite the lack of revenue growth, the stock has returned a solid 92% the last twelve months. To us that means that there isn't a lot of correlation between the past revenue performance and the share price, but a closer look at analyst forecasts and the bottom line may well explain a lot.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

Take a more thorough look at WCT Holdings Berhad's financial health with this free report on its balance sheet.

A Different Perspective

It's good to see that WCT Holdings Berhad has rewarded shareholders with a total shareholder return of 92% in the last twelve months. That's better than the annualised return of 5% over half a decade, implying that the company is doing better recently. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with WCT Holdings Berhad (at least 1 which shouldn't be ignored) , and understanding them should be part of your investment process.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Malaysian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if WCT Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:WCT

WCT Holdings Berhad

An investment holding company, engages in engineering and construction, property development, and property investment and management activities in Malaysia, the Middle East, and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor