- Malaysia

- /

- Industrials

- /

- KLSE:TEXCHEM

Downgrade: Here's How This Analyst Sees Texchem Resources Bhd (KLSE:TEXCHEM) Performing In The Near Term

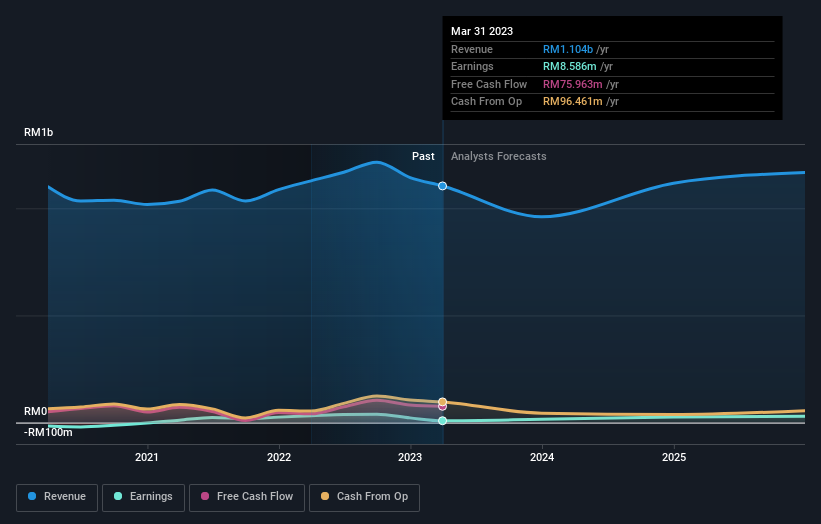

Market forces rained on the parade of Texchem Resources Bhd (KLSE:TEXCHEM) shareholders today, when the covering analyst downgraded their forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analyst seeing grey clouds on the horizon.

Following the latest downgrade, the current consensus, from the sole analyst covering Texchem Resources Bhd, is for revenues of RM960m in 2023, which would reflect a definite 13% reduction in Texchem Resources Bhd's sales over the past 12 months. Statutory earnings per share are presumed to bounce 64% to RM0.12. Before this latest update, the analyst had been forecasting revenues of RM1.2b and earnings per share (EPS) of RM0.31 in 2023. Indeed, we can see that the analyst is a lot more bearish about Texchem Resources Bhd's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

See our latest analysis for Texchem Resources Bhd

The consensus price target fell 23% to RM2.77, with the weaker earnings outlook clearly leading analyst valuation estimates.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. Over the past five years, revenues have declined around 0.2% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 13% decline in revenue until the end of 2023. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 3.1% annually. So it's pretty clear that, while it does have declining revenues, the analyst also expect Texchem Resources Bhd to suffer worse than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that the analyst has reduced their earnings per share estimates, suggesting business headwinds lay ahead for Texchem Resources Bhd. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. After such a stark change in sentiment from the analyst, we'd understand if readers now felt a bit wary of Texchem Resources Bhd.

There might be good reason for analyst bearishness towards Texchem Resources Bhd, like its declining profit margins. Learn more, and discover the 4 other risks we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Texchem Resources Bhd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TEXCHEM

Texchem Resources Bhd

An investment holding company, engages in industrial, polymer engineering, food, restaurant, and venture businesses.

Good value with moderate growth potential.

Market Insights

Community Narratives