Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Ta Win Holdings Berhad (KLSE:TAWIN) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Ta Win Holdings Berhad

What Is Ta Win Holdings Berhad's Debt?

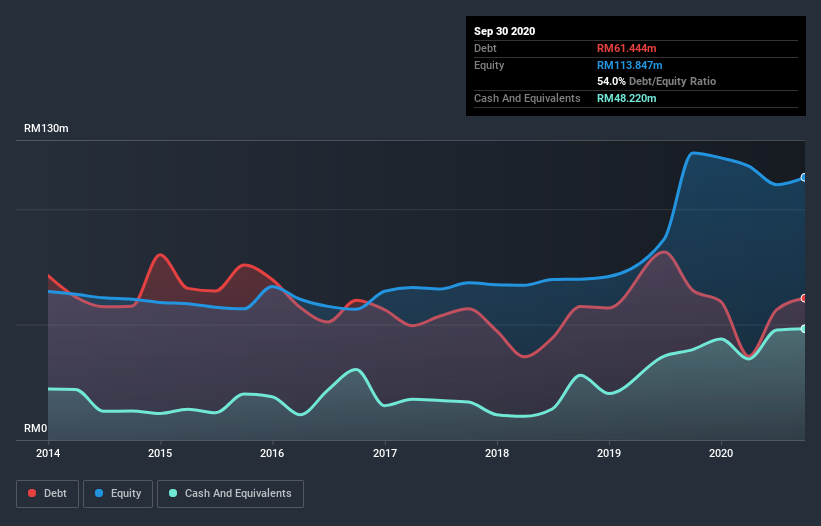

The image below, which you can click on for greater detail, shows that Ta Win Holdings Berhad had debt of RM61.4m at the end of September 2020, a reduction from RM64.9m over a year. However, because it has a cash reserve of RM48.2m, its net debt is less, at about RM13.2m.

How Healthy Is Ta Win Holdings Berhad's Balance Sheet?

The latest balance sheet data shows that Ta Win Holdings Berhad had liabilities of RM72.3m due within a year, and liabilities of RM7.60m falling due after that. On the other hand, it had cash of RM48.2m and RM50.3m worth of receivables due within a year. So it actually has RM18.7m more liquid assets than total liabilities.

This surplus suggests that Ta Win Holdings Berhad is using debt in a way that is appears to be both safe and conservative. Due to its strong net asset position, it is not likely to face issues with its lenders. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Ta Win Holdings Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Ta Win Holdings Berhad had a loss before interest and tax, and actually shrunk its revenue by 24%, to RM270m. That makes us nervous, to say the least.

Caveat Emptor

While Ta Win Holdings Berhad's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost a very considerable RM14m at the EBIT level. On a more positive note, the company does have liquid assets, so it has a bit of time to improve its operations before the debt becomes an acute problem. But a profit would do more to inspire us to research the business more closely. This one is a bit too risky for our liking. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 5 warning signs for Ta Win Holdings Berhad you should be aware of, and 1 of them shouldn't be ignored.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading Ta Win Holdings Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Ta Win Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:TAWIN

Ta Win Holdings Berhad

An investment holding company, manufactures, sells, and trades in copper wires, rods, and related products in Malaysia, Brunei, Hong Kong, China, Vietnam, and internationally.

Adequate balance sheet low.

Market Insights

Community Narratives