TAS Offshore Berhad (KLSE:TAS) Stock Rockets 33% But Many Are Still Ignoring The Company

The TAS Offshore Berhad (KLSE:TAS) share price has done very well over the last month, posting an excellent gain of 33%. The annual gain comes to 168% following the latest surge, making investors sit up and take notice.

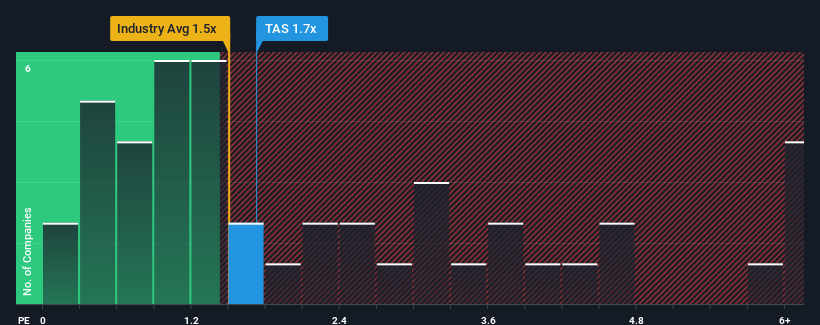

Even after such a large jump in price, you could still be forgiven for feeling indifferent about TAS Offshore Berhad's P/S ratio of 1.7x, since the median price-to-sales (or "P/S") ratio for the Machinery industry in Malaysia is also close to 1.5x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

See our latest analysis for TAS Offshore Berhad

How TAS Offshore Berhad Has Been Performing

TAS Offshore Berhad's revenue growth of late has been pretty similar to most other companies. It seems that many are expecting the mediocre revenue performance to persist, which has held the P/S ratio back. If you like the company, you'd be hoping this can at least be maintained so that you could pick up some stock while it's not quite in favour.

Keen to find out how analysts think TAS Offshore Berhad's future stacks up against the industry? In that case, our free report is a great place to start.Is There Some Revenue Growth Forecasted For TAS Offshore Berhad?

In order to justify its P/S ratio, TAS Offshore Berhad would need to produce growth that's similar to the industry.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. Despite the lack of growth, the company was still able to deliver immense revenue growth over the last three years. So while the company has done a great job in the past, it's somewhat concerning to see revenue growth decline so harshly.

Looking ahead now, revenue is anticipated to climb by 56% during the coming year according to the lone analyst following the company. Meanwhile, the rest of the industry is forecast to only expand by 30%, which is noticeably less attractive.

In light of this, it's curious that TAS Offshore Berhad's P/S sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Key Takeaway

TAS Offshore Berhad appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Despite enticing revenue growth figures that outpace the industry, TAS Offshore Berhad's P/S isn't quite what we'd expect. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. This uncertainty seems to be reflected in the share price which, while stable, could be higher given the revenue forecasts.

You should always think about risks. Case in point, we've spotted 5 warning signs for TAS Offshore Berhad you should be aware of, and 2 of them can't be ignored.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

If you're looking to trade TAS Offshore Berhad, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if TAS Offshore Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TAS

TAS Offshore Berhad

An investment holding company, engages in the shipbuilding and ship repairing activities in Malaysia, Singapore, and Indonesia.

Flawless balance sheet and good value.

Market Insights

Community Narratives