Advertisement

After Leaping 43% TAS Offshore Berhad (KLSE:TAS) Shares Are Not Flying Under The Radar

Despite an already strong run, TAS Offshore Berhad (KLSE:TAS) shares have been powering on, with a gain of 43% in the last thirty days. The last month tops off a massive increase of 288% in the last year.

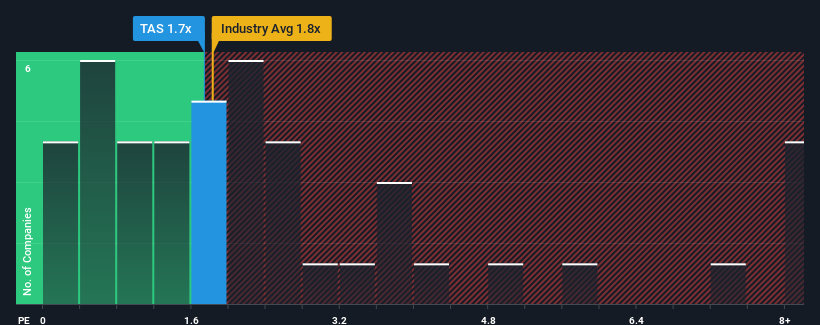

Even after such a large jump in price, there still wouldn't be many who think TAS Offshore Berhad's price-to-sales (or "P/S") ratio of 1.7x is worth a mention when the median P/S in Malaysia's Machinery industry is similar at about 1.8x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

See our latest analysis for TAS Offshore Berhad

What Does TAS Offshore Berhad's P/S Mean For Shareholders?

Recent times have been advantageous for TAS Offshore Berhad as its revenues have been rising faster than most other companies. One possibility is that the P/S ratio is moderate because investors think this strong revenue performance might be about to tail off. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on TAS Offshore Berhad will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For TAS Offshore Berhad?

There's an inherent assumption that a company should be matching the industry for P/S ratios like TAS Offshore Berhad's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 63% last year. The strong recent performance means it was also able to grow revenue by 251% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 24% during the coming year according to the lone analyst following the company. Meanwhile, the rest of the industry is forecast to expand by 26%, which is not materially different.

With this information, we can see why TAS Offshore Berhad is trading at a fairly similar P/S to the industry. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Key Takeaway

Its shares have lifted substantially and now TAS Offshore Berhad's P/S is back within range of the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've seen that TAS Offshore Berhad maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won't throw up any surprises. Unless these conditions change, they will continue to support the share price at these levels.

You should always think about risks. Case in point, we've spotted 5 warning signs for TAS Offshore Berhad you should be aware of, and 2 of them shouldn't be ignored.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if TAS Offshore Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TAS

TAS Offshore Berhad

An investment holding company, engages in the shipbuilding and ship repairing activities in Malaysia, Singapore, and Indonesia.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor