Advertisement

Does SKB Shutters Corporation Berhad (KLSE:SKBSHUT) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that SKB Shutters Corporation Berhad (KLSE:SKBSHUT) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for SKB Shutters Corporation Berhad

What Is SKB Shutters Corporation Berhad's Debt?

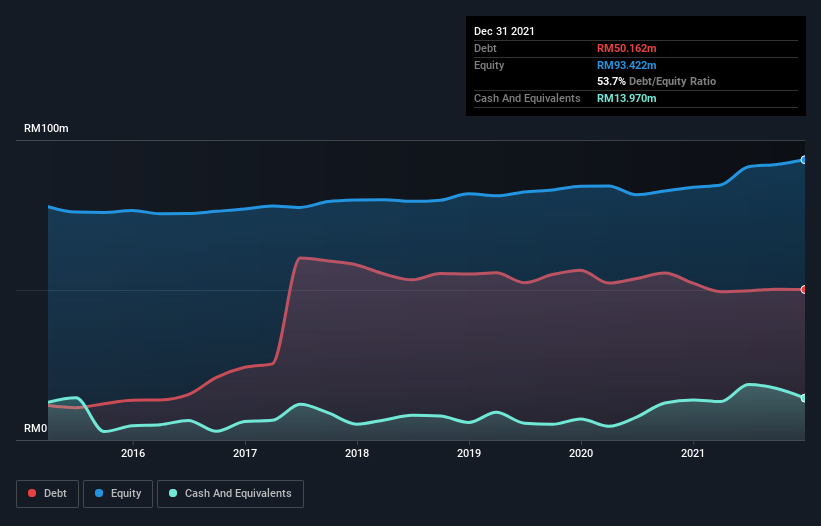

You can click the graphic below for the historical numbers, but it shows that SKB Shutters Corporation Berhad had RM50.2m of debt in December 2021, down from RM52.3m, one year before. On the flip side, it has RM14.0m in cash leading to net debt of about RM36.2m.

How Healthy Is SKB Shutters Corporation Berhad's Balance Sheet?

According to the last reported balance sheet, SKB Shutters Corporation Berhad had liabilities of RM41.8m due within 12 months, and liabilities of RM38.0m due beyond 12 months. On the other hand, it had cash of RM14.0m and RM23.9m worth of receivables due within a year. So its liabilities total RM42.0m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of RM45.5m, so it does suggest shareholders should keep an eye on SKB Shutters Corporation Berhad's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

SKB Shutters Corporation Berhad has a debt to EBITDA ratio of 3.7 and its EBIT covered its interest expense 4.1 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. The silver lining is that SKB Shutters Corporation Berhad grew its EBIT by 126% last year, which nourishing like the idealism of youth. If that earnings trend continues it will make its debt load much more manageable in the future. The balance sheet is clearly the area to focus on when you are analysing debt. But it is SKB Shutters Corporation Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, SKB Shutters Corporation Berhad actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Both SKB Shutters Corporation Berhad's ability to to convert EBIT to free cash flow and its EBIT growth rate gave us comfort that it can handle its debt. On the other hand, its level of total liabilities makes us a little less comfortable about its debt. Considering this range of data points, we think SKB Shutters Corporation Berhad is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for SKB Shutters Corporation Berhad that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SKBSHUT

SKB Shutters Corporation Berhad

An investment holding company, engages in the manufacture, sale, and trade of roller shutters, racking systems, storage systems, and related steel products in Malaysia, Asia, Oceania, the Middle East, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor