Advertisement

Kobay Technology Bhd (KLSE:KOBAY) Takes On Some Risk With Its Use Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Kobay Technology Bhd. (KLSE:KOBAY) makes use of debt. But the more important question is: how much risk is that debt creating?

We've discovered 1 warning sign about Kobay Technology Bhd. View them for free.When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

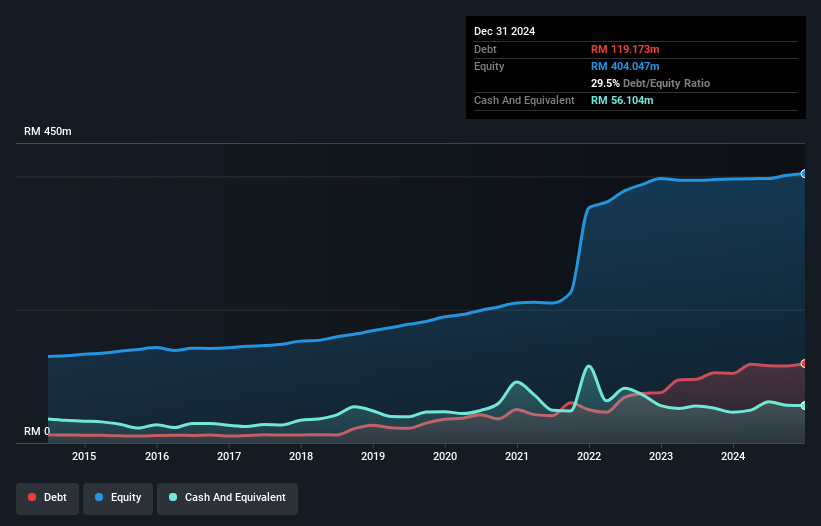

What Is Kobay Technology Bhd's Debt?

The image below, which you can click on for greater detail, shows that at December 2024 Kobay Technology Bhd had debt of RM119.2m, up from RM104.3m in one year. However, it does have RM56.1m in cash offsetting this, leading to net debt of about RM63.1m.

How Strong Is Kobay Technology Bhd's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Kobay Technology Bhd had liabilities of RM153.3m due within 12 months and liabilities of RM52.3m due beyond that. Offsetting this, it had RM56.1m in cash and RM88.3m in receivables that were due within 12 months. So its liabilities total RM61.1m more than the combination of its cash and short-term receivables.

Given Kobay Technology Bhd has a market capitalization of RM445.1m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

Check out our latest analysis for Kobay Technology Bhd

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Kobay Technology Bhd's net debt is sitting at a very reasonable 1.7 times its EBITDA, while its EBIT covered its interest expense just 3.9 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. If Kobay Technology Bhd can keep growing EBIT at last year's rate of 13% over the last year, then it will find its debt load easier to manage. There's no doubt that we learn most about debt from the balance sheet. But it is Kobay Technology Bhd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, Kobay Technology Bhd burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Kobay Technology Bhd's struggle to convert EBIT to free cash flow had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. But on the bright side, its ability to to grow its EBIT isn't too shabby at all. Looking at all the angles mentioned above, it does seem to us that Kobay Technology Bhd is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 1 warning sign for Kobay Technology Bhd that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Kobay Technology Bhd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KOBAY

Kobay Technology Bhd

An investment holding company, engages in the manufacturing, property development, pharmaceutical and healthcare, and asset management businesses in Malaysia, Singapore, the United States, and internationally.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor