- Malaysia

- /

- Construction

- /

- KLSE:INGENIEU

Ingenieur Gudang Berhad (KLSE:INGENIEU) Not Doing Enough For Some Investors As Its Shares Slump 28%

Ingenieur Gudang Berhad (KLSE:INGENIEU) shares have had a horrible month, losing 28% after a relatively good period beforehand. Looking back over the past twelve months the stock has been a solid performer regardless, with a gain of 15%.

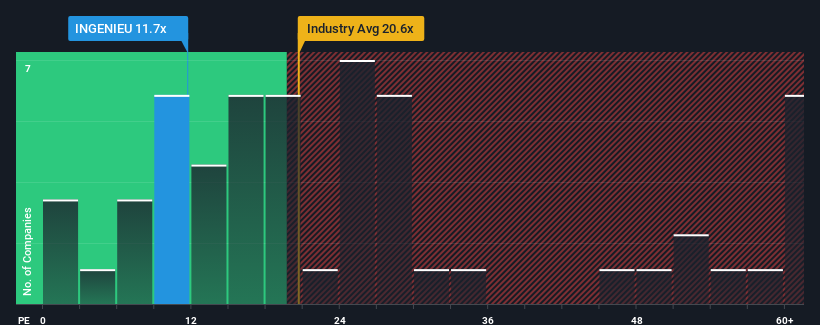

Even after such a large drop in price, Ingenieur Gudang Berhad's price-to-earnings (or "P/E") ratio of 11.7x might still make it look like a buy right now compared to the market in Malaysia, where around half of the companies have P/E ratios above 17x and even P/E's above 29x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

For example, consider that Ingenieur Gudang Berhad's financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

View our latest analysis for Ingenieur Gudang Berhad

Is There Any Growth For Ingenieur Gudang Berhad?

In order to justify its P/E ratio, Ingenieur Gudang Berhad would need to produce sluggish growth that's trailing the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 54%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Comparing that to the market, which is predicted to deliver 17% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

In light of this, it's understandable that Ingenieur Gudang Berhad's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

What We Can Learn From Ingenieur Gudang Berhad's P/E?

Ingenieur Gudang Berhad's recently weak share price has pulled its P/E below most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Ingenieur Gudang Berhad revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

You need to take note of risks, for example - Ingenieur Gudang Berhad has 6 warning signs (and 1 which is concerning) we think you should know about.

If you're unsure about the strength of Ingenieur Gudang Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

If you're looking to trade Ingenieur Gudang Berhad, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:INGENIEU

Ingenieur Gudang Berhad

An investment holding company, engages in construction activities in Malaysia.

Excellent balance sheet with acceptable track record.

Market Insights

Community Narratives