Advertisement

- Malaysia

- /

- Trade Distributors

- /

- KLSE:DANCO

Dancomech Holdings Berhad (KLSE:DANCO) Stock Has Shown Weakness Lately But Financials Look Strong: Should Prospective Shareholders Make The Leap?

With its stock down 5.0% over the past week, it is easy to disregard Dancomech Holdings Berhad (KLSE:DANCO). But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. In this article, we decided to focus on Dancomech Holdings Berhad's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

Check out our latest analysis for Dancomech Holdings Berhad

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Dancomech Holdings Berhad is:

10% = RM15m ÷ RM148m (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. So, this means that for every MYR1 of its shareholder's investments, the company generates a profit of MYR0.10.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Dancomech Holdings Berhad's Earnings Growth And 10% ROE

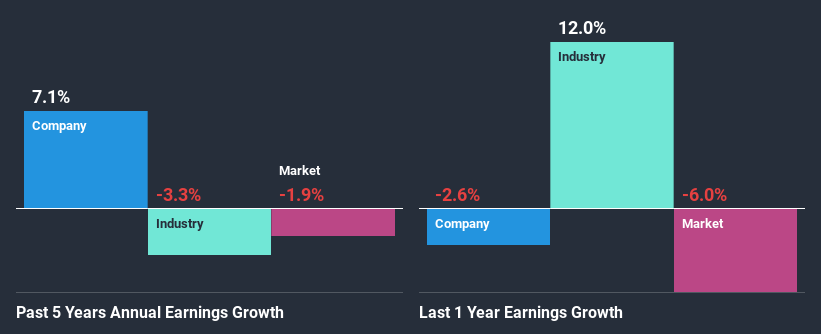

When you first look at it, Dancomech Holdings Berhad's ROE doesn't look that attractive. However, the fact that the its ROE is quite higher to the industry average of 5.1% doesn't go unnoticed by us. Consequently, this likely laid the ground for the decent growth of 7.1% seen over the past five years by Dancomech Holdings Berhad. Bear in mind, the company does have a moderately low ROE. It is just that the industry ROE is lower. Hence there might be some other aspects that are causing earnings to grow. For example, it is possible that the broader industry is going through a high growth phase, or that the company has a low payout ratio.

When you consider the fact that the industry earnings have shrunk at a rate of 3.3% in the same period, the company's net income growth is pretty remarkable.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Dancomech Holdings Berhad is trading on a high P/E or a low P/E, relative to its industry.

Is Dancomech Holdings Berhad Using Its Retained Earnings Effectively?

Dancomech Holdings Berhad has a healthy combination of a moderate three-year median payout ratio of 36% (or a retention ratio of 64%) and a respectable amount of growth in earnings as we saw above, meaning that the company has been making efficient use of its profits.

Moreover, Dancomech Holdings Berhad is determined to keep sharing its profits with shareholders which we infer from its long history of four years of paying a dividend.

Summary

In total, we are pretty happy with Dancomech Holdings Berhad's performance. In particular, it's great to see that the company has seen significant growth in its earnings backed by a respectable ROE and a high reinvestment rate. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

If you’re looking to trade Dancomech Holdings Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:DANCO

Dancomech Holdings Berhad

An investment holding company, trades in and distributes process control equipment, measurement instruments, and industrial pumps in Malaysia, Indonesia, and internationally.

Undervalued with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor