- Malaysia

- /

- Trade Distributors

- /

- KLSE:BCMALL

Slammed 33% BCM Alliance Berhad (KLSE:BCMALL) Screens Well Here But There Might Be A Catch

The BCM Alliance Berhad (KLSE:BCMALL) share price has fared very poorly over the last month, falling by a substantial 33%. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 33% in that time.

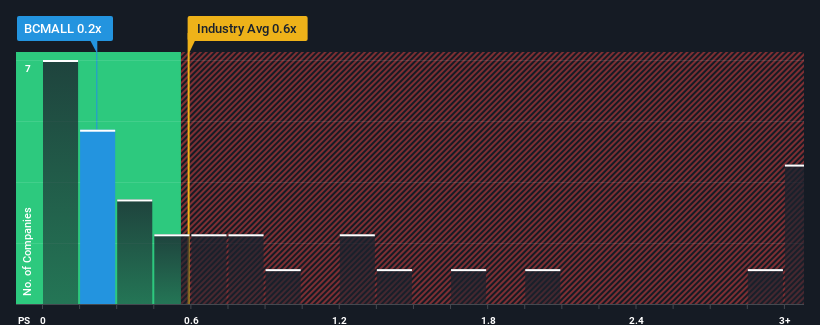

In spite of the heavy fall in price, it's still not a stretch to say that BCM Alliance Berhad's price-to-sales (or "P/S") ratio of 0.2x right now seems quite "middle-of-the-road" compared to the Trade Distributors industry in Malaysia, where the median P/S ratio is around 0.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for BCM Alliance Berhad

How BCM Alliance Berhad Has Been Performing

BCM Alliance Berhad has been doing a decent job lately as it's been growing revenue at a reasonable pace. Perhaps the expectation moving forward is that the revenue growth will track in line with the wider industry for the near term, which has kept the P/S subdued. Those who are bullish on BCM Alliance Berhad will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on BCM Alliance Berhad's earnings, revenue and cash flow.How Is BCM Alliance Berhad's Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like BCM Alliance Berhad's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 3.5% last year. Pleasingly, revenue has also lifted 38% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

When compared to the industry's one-year growth forecast of 7.6%, the most recent medium-term revenue trajectory is noticeably more alluring

In light of this, it's curious that BCM Alliance Berhad's P/S sits in line with the majority of other companies. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Bottom Line On BCM Alliance Berhad's P/S

BCM Alliance Berhad's plummeting stock price has brought its P/S back to a similar region as the rest of the industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that BCM Alliance Berhad currently trades on a lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. When we see strong revenue with faster-than-industry growth, we can only assume potential risks are what might be placing pressure on the P/S ratio. It appears some are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

We don't want to rain on the parade too much, but we did also find 3 warning signs for BCM Alliance Berhad that you need to be mindful of.

If you're unsure about the strength of BCM Alliance Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if BCM Alliance Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KLSE:BCMALL

BCM Alliance Berhad

An investment holding company, distributes commercial laundry equipment, medical devices, and healthcare products in Malaysia and internationally.

Flawless balance sheet low.