When International Hotel Investments p.l.c. (MTSE:IHI) reported its results to December 2020 its auditors, PricewaterhouseCoopers LLP could not be sure that it would be able to continue as a going concern in the next year. Thus we can say that, based on the results to that date, the company should raise capital or otherwise raise cash, without much delay.

If the company does have to issue more shares, potential investors will be sure to consider how desperate it is for capital. So shareholders should absolutely be taking a close look at how risky the balance sheet is. The big consideration is whether it can repay its debt, since in the worst case scenario, creditors could force the company to bankruptcy.

Check out our latest analysis for International Hotel Investments

What Is International Hotel Investments's Debt?

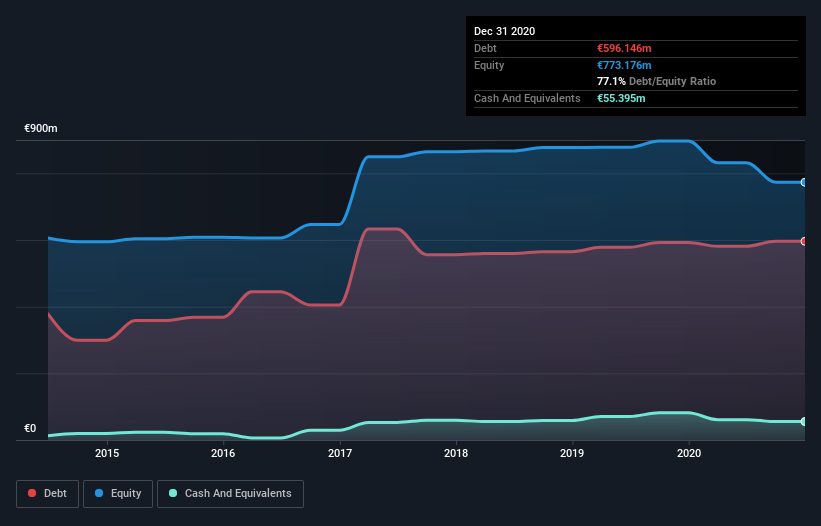

As you can see below, International Hotel Investments had €596.1m of debt, at December 2020, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of €55.4m, its net debt is less, at about €540.8m.

A Look At International Hotel Investments' Liabilities

According to the last reported balance sheet, International Hotel Investments had liabilities of €119.7m due within 12 months, and liabilities of €651.2m due beyond 12 months. Offsetting these obligations, it had cash of €55.4m as well as receivables valued at €34.7m due within 12 months. So its liabilities total €680.8m more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the €384.8m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, International Hotel Investments would probably need a major re-capitalization if its creditors were to demand repayment. There's no doubt that we learn most about debt from the balance sheet. But it is International Hotel Investments's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, International Hotel Investments made a loss at the EBIT level, and saw its revenue drop to €92m, which is a fall of 66%. That makes us nervous, to say the least.

Caveat Emptor

Not only did International Hotel Investments's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost a very considerable €40m at the EBIT level. When we look at that alongside the significant liabilities, we're not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through €17m in negative free cash flow over the last year. So suffice it to say we consider the stock to be risky. We prefer to avoid a company after its auditor has expressed any uncertainty about its ability to continue as a going concern. That's because we find it more comfortable to invest in companies that always keep the balance sheet reasonably strong. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example - International Hotel Investments has 1 warning sign we think you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade International Hotel Investments, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About MTSE:IHI

International Hotel Investments

Engages in the ownership, development, and operation of hotels, leisure facilities, and other activities related to the tourism industry and commercial centres.

Low with questionable track record.

Market Insights

Community Narratives