- South Korea

- /

- Logistics

- /

- KOSE:A086280

Hyundai Glovis Co., Ltd. (KRX:086280) Stock Has Shown Weakness Lately But Financials Look Strong: Should Prospective Shareholders Make The Leap?

With its stock down 9.0% over the past week, it is easy to disregard Hyundai Glovis (KRX:086280). However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. In this article, we decided to focus on Hyundai Glovis' ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for Hyundai Glovis

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Hyundai Glovis is:

14% = ₩667b ÷ ₩4.9t (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. So, this means that for every ₩1 of its shareholder's investments, the company generates a profit of ₩0.14.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Hyundai Glovis' Earnings Growth And 14% ROE

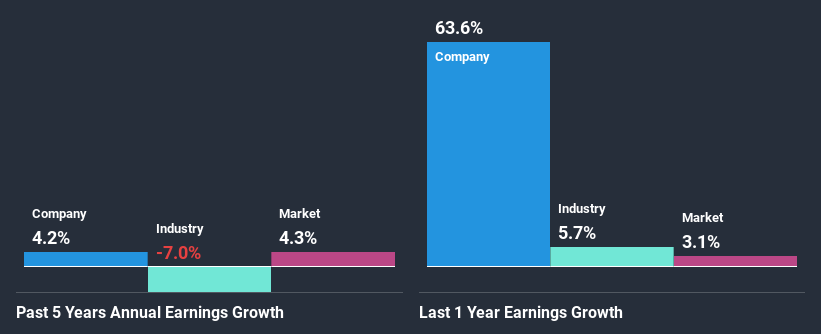

At first glance, Hyundai Glovis seems to have a decent ROE. Further, the company's ROE compares quite favorably to the industry average of 4.5%. Despite this, Hyundai Glovis' five year net income growth was quite low averaging at only 4.2%. That's a bit unexpected from a company which has such a high rate of return. A few likely reasons why this could happen is that the company could have a high payout ratio or the business has allocated capital poorly, for instance.

Next, on comparing with the industry net income growth, we found that the growth figure reported by Hyundai Glovis compares quite favourably to the industry average, which shows a decline of 7.0% in the same period.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Hyundai Glovis is trading on a high P/E or a low P/E, relative to its industry.

Is Hyundai Glovis Making Efficient Use Of Its Profits?

Hyundai Glovis has a low three-year median payout ratio of 24% (meaning, the company keeps the remaining 76% of profits) which means that the company is retaining more of its earnings. However, the low earnings growth number doesn't reflect this as high growth usually follows high profit retention. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

Additionally, Hyundai Glovis has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 20%. Accordingly, forecasts suggest that Hyundai Glovis' future ROE will be 12% which is again, similar to the current ROE.

Conclusion

Overall, we are quite pleased with Hyundai Glovis' performance. Particularly, we like that the company is reinvesting heavily into its business, and at a high rate of return. Unsurprisingly, this has led to an impressive earnings growth. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

When trading Hyundai Glovis or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hyundai Glovis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A086280

Hyundai Glovis

Operates as logistics and distribution company in South Korea and internationally.

Flawless balance sheet and undervalued.