Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSE:A007810

Global Stocks Estimated To Be Trading Below Intrinsic Value By Up To 43.3%

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to navigate the complexities of interest rate expectations and economic indicators, investors are keenly watching for opportunities amid fluctuating indices. With major U.S. stock indexes reaching new highs driven by AI optimism and anticipated Federal Reserve rate cuts, the search for stocks trading below their intrinsic value becomes increasingly relevant. In such an environment, a good stock is often characterized by its potential to deliver value despite broader market trends, offering investors a chance to capitalize on perceived undervaluations.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Micro Systemation (OM:MSAB B) | SEK61.40 | SEK122.64 | 49.9% |

| Kuraray (TSE:3405) | ¥1756.00 | ¥3488.37 | 49.7% |

| Kolmar Korea (KOSE:A161890) | ₩78700.00 | ₩156214.35 | 49.6% |

| Inner Mongolia Xingye Silver&Tin MiningLtd (SZSE:000426) | CN¥25.61 | CN¥50.97 | 49.8% |

| Gofore Oyj (HLSE:GOFORE) | €14.88 | €29.64 | 49.8% |

| Food Empire Holdings (SGX:F03) | SGD2.59 | SGD5.16 | 49.8% |

| Faraday Technology (TWSE:3035) | NT$150.00 | NT$299.86 | 50% |

| Dogus Otomotiv Servis ve Ticaret (IBSE:DOAS) | TRY169.60 | TRY336.86 | 49.7% |

| Brockhaus Technologies (XTRA:BKHT) | €9.64 | €19.22 | 49.8% |

| Alfio Bardolla Training Group (BIT:ABTG) | €1.91 | €3.79 | 49.6% |

Let's dive into some prime choices out of the screener.

Fertiglobe (ADX:FERTIGLB)

Overview: Fertiglobe plc, along with its subsidiaries, is engaged in the production and sale of nitrogen-based products across Europe, North and South America, Africa, the Middle East, Asia, and Oceania with a market capitalization of AED20.41 billion.

Operations: Fertiglobe's revenue is primarily derived from the production and marketing of owned produced volumes, amounting to $2.03 billion, and third-party trading activities, which contribute $193.80 million.

Estimated Discount To Fair Value: 17.1%

Fertiglobe's current trading price of AED2.46 is below its estimated fair value of AED2.97, indicating potential undervaluation based on cash flows. Despite a high debt level and slower revenue growth forecast compared to the AE market, earnings are expected to grow significantly at 23.8% annually, surpassing market averages. However, profit margins have declined from last year and dividends are not well covered by earnings, raising concerns about financial sustainability in the short term.

- According our earnings growth report, there's an indication that Fertiglobe might be ready to expand.

- Click here to discover the nuances of Fertiglobe with our detailed financial health report.

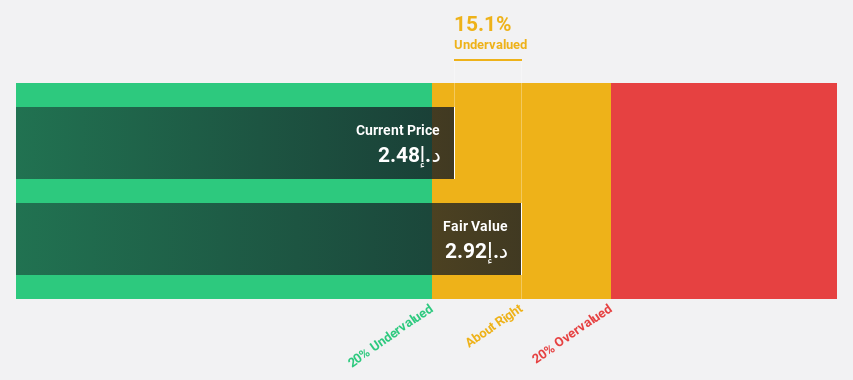

Korea Circuit (KOSE:A007810)

Overview: Korea Circuit Co., Ltd. produces and sells printed circuit boards globally, with a market cap of ₩436.45 billion.

Operations: The company generates revenue primarily from the manufacture of printed circuit boards, totaling ₩1.36 billion.

Estimated Discount To Fair Value: 43.3%

Korea Circuit's current price of ₩17,490 is significantly below its estimated fair value of ₩30,828.76, highlighting potential undervaluation. Although revenue growth is modest at 7.3% annually, it outpaces the KR market average and the company is expected to become profitable within three years with earnings growth forecasted at 88.67% per year. Despite a low projected return on equity of 11.6%, Korea Circuit offers good relative value compared to peers and industry standards.

- Upon reviewing our latest growth report, Korea Circuit's projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of Korea Circuit stock in this financial health report.

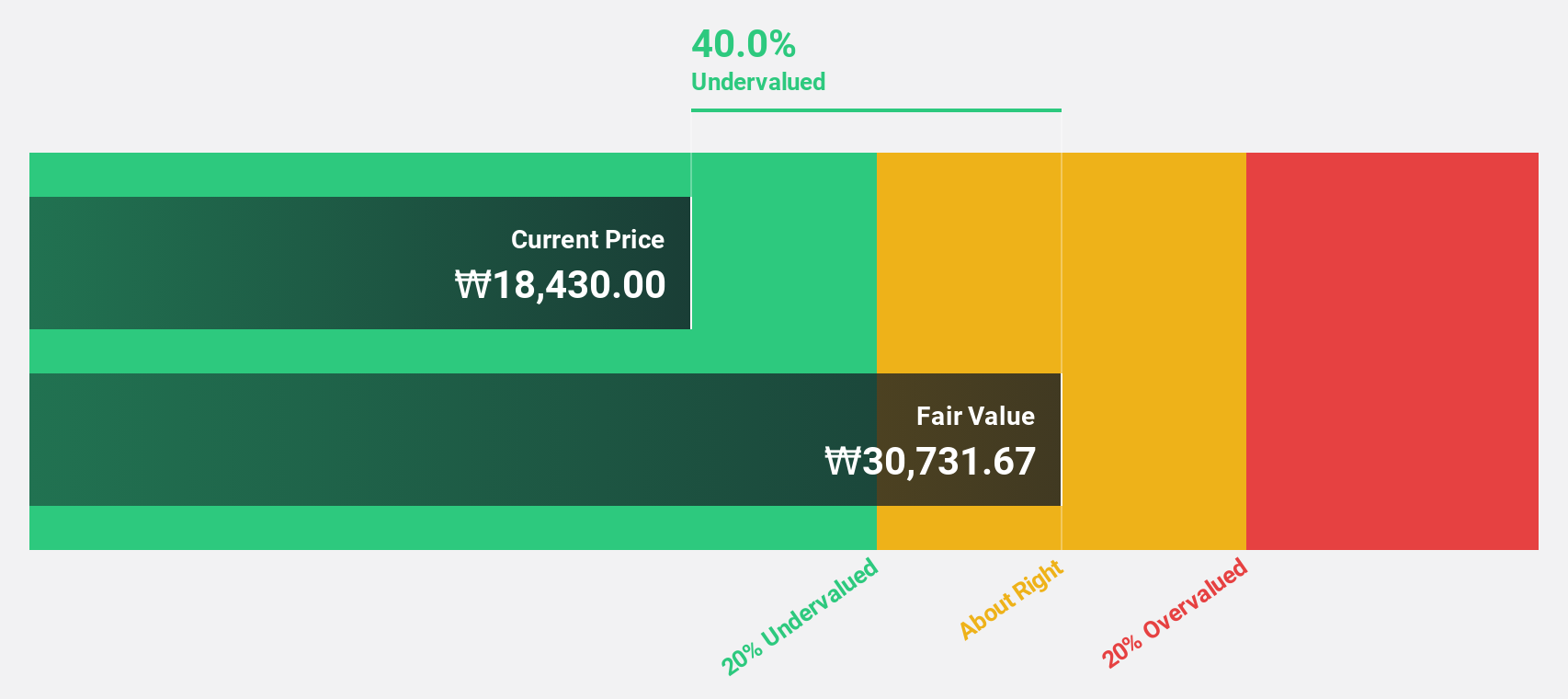

Cal-Comp Electronics (Thailand) (SET:CCET)

Overview: Cal-Comp Electronics (Thailand) Public Company Limited, along with its subsidiaries, manufactures electronic products globally and has a market cap of THB63.22 billion.

Operations: The company's revenue is primarily derived from its Computer Peripheral segment at THB161.78 billion and Telecommunication Products at THB23.83 billion, with additional income from Service Income amounting to THB1.71 billion.

Estimated Discount To Fair Value: 21.3%

Cal-Comp Electronics (Thailand) is trading at a discount, with its current price below the estimated fair value of THB 7.69, indicating potential undervaluation based on cash flows. Despite a high debt level and declining recent sales, its earnings are forecast to grow significantly at 20.4% annually, outpacing the Thai market average. The company has declared an interim dividend of THB 0.07 per share for the first half of 2025, reflecting stable cash flow management amidst fluctuating revenues.

- Our earnings growth report unveils the potential for significant increases in Cal-Comp Electronics (Thailand)'s future results.

- Get an in-depth perspective on Cal-Comp Electronics (Thailand)'s balance sheet by reading our health report here.

Seize The Opportunity

- Delve into our full catalog of 516 Undervalued Global Stocks Based On Cash Flows here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Korea Circuit might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A007810

Korea Circuit

Engages in the production and sale of printed circuit boards worldwide.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor