Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSE:A007660

Asian Market Stocks That May Be Trading Below Estimated Value

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, the Asian markets have shown resilience amidst global economic uncertainties, with Chinese stocks seeing a rise due to hopes for more stimulus in response to persistent deflation. As investors navigate these fluctuating conditions, identifying stocks that may be trading below their estimated value can offer potential opportunities for those looking to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| SILICON2 (KOSDAQ:A257720) | ₩52800.00 | ₩104187.44 | 49.3% |

| Range Intelligent Computing Technology Group (SZSE:300442) | CN¥52.55 | CN¥103.62 | 49.3% |

| Peijia Medical (SEHK:9996) | HK$7.93 | HK$15.57 | 49.1% |

| Nanya New Material TechnologyLtd (SHSE:688519) | CN¥42.94 | CN¥85.38 | 49.7% |

| Medy-Tox (KOSDAQ:A086900) | ₩162200.00 | ₩322233.66 | 49.7% |

| Mandom (TSE:4917) | ¥1419.00 | ¥2835.57 | 50% |

| Livero (TSE:9245) | ¥1727.00 | ¥3430.34 | 49.7% |

| Hugel (KOSDAQ:A145020) | ₩355000.00 | ₩698441.84 | 49.2% |

| HL Holdings (KOSE:A060980) | ₩41500.00 | ₩82181.95 | 49.5% |

| ALUX (KOSDAQ:A475580) | ₩11500.00 | ₩22593.59 | 49.1% |

Let's review some notable picks from our screened stocks.

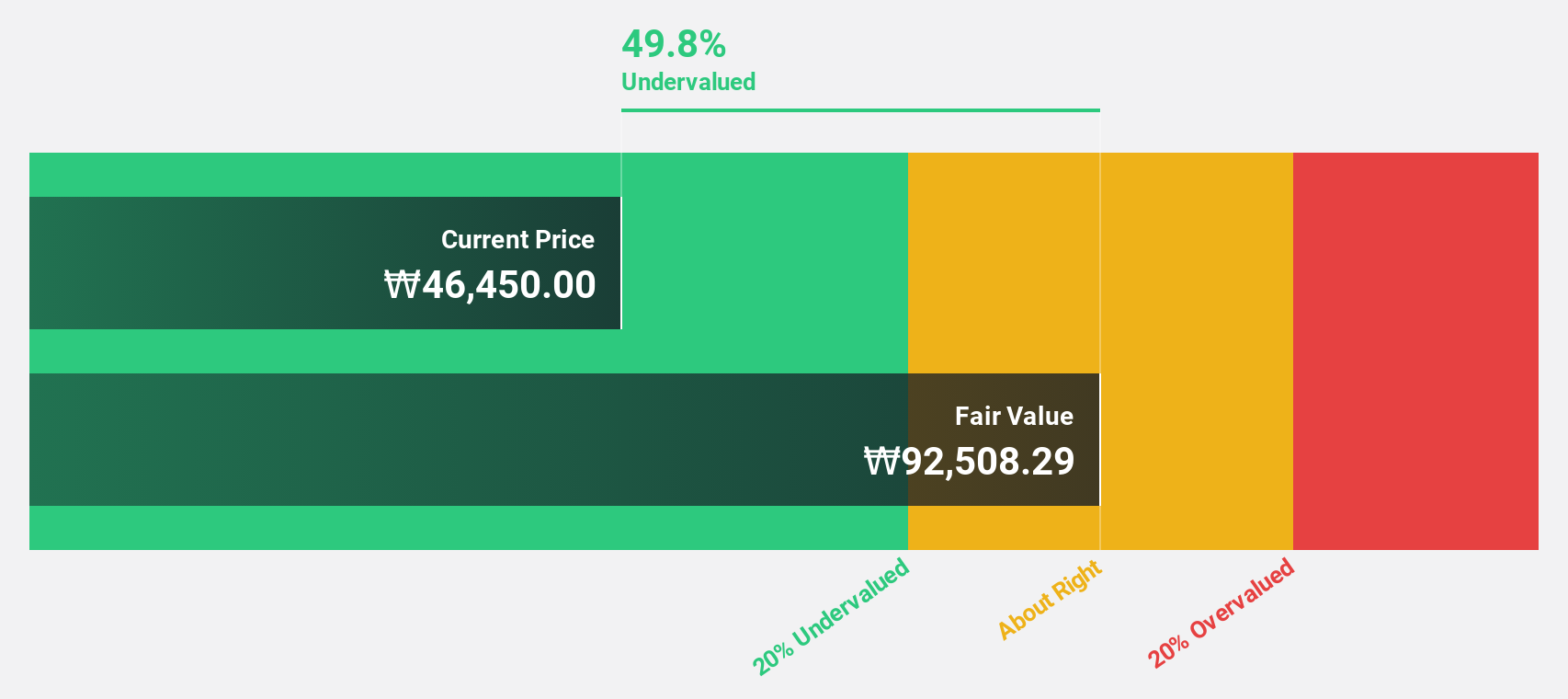

ISU Petasys (KOSE:A007660)

Overview: ISU Petasys Co., Ltd. manufactures and sells printed circuit boards (PCBs) globally, with a market capitalization of approximately ₩4.43 trillion.

Operations: The company's revenue primarily comes from the manufacture and sale of printed circuit boards, amounting to approximately ₩889.75 billion.

Estimated Discount To Fair Value: 26%

ISU Petasys is trading at ₩60,400, 26% below its estimated fair value of ₩81,676.04. Despite recent shareholder dilution and high debt levels, the company shows promising growth prospects with forecasted earnings growth of 28.4% per year and revenue growth of 18.3% per year, both surpassing the Korean market averages. However, its share price has been highly volatile recently, which may concern some investors focusing on stability.

- According our earnings growth report, there's an indication that ISU Petasys might be ready to expand.

- Click here and access our complete balance sheet health report to understand the dynamics of ISU Petasys.

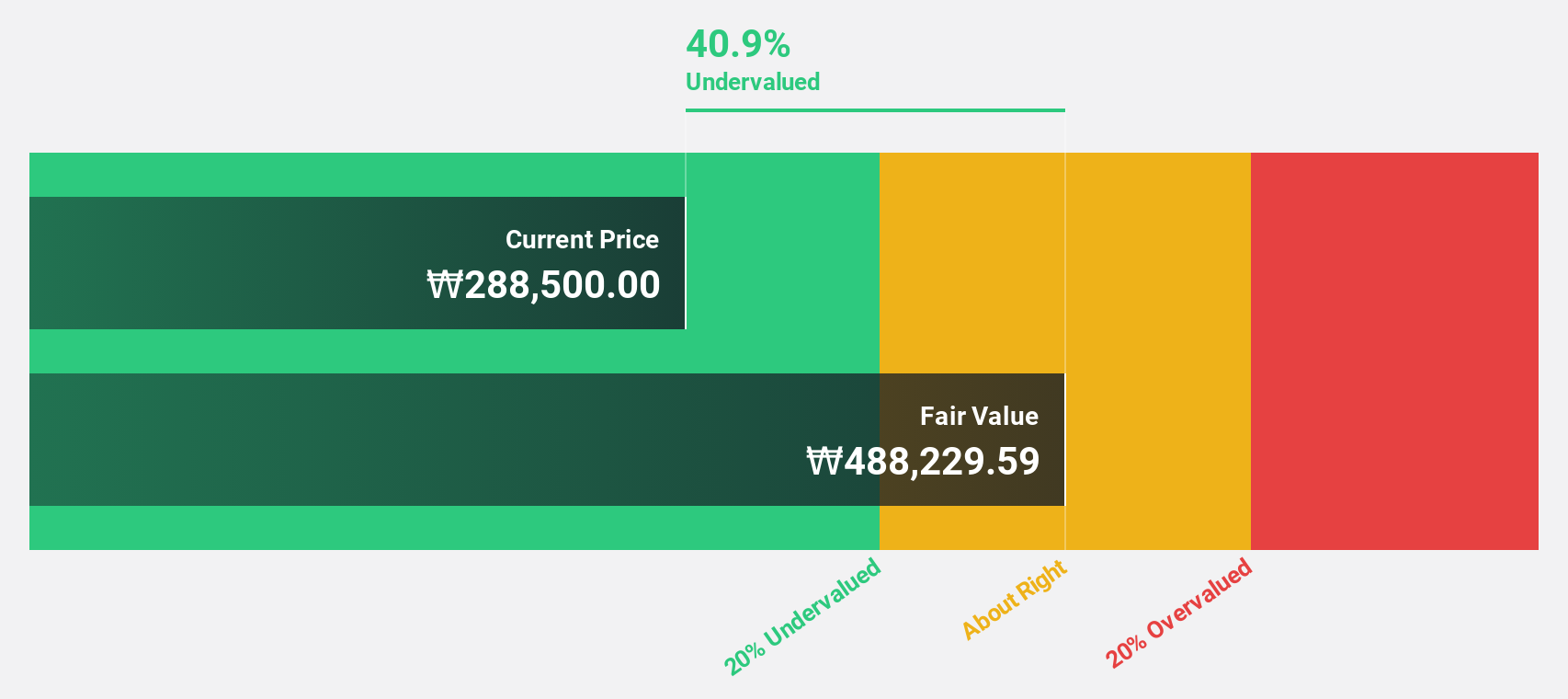

Hanmi Pharm (KOSE:A128940)

Overview: Hanmi Pharm Co., Ltd. is a biopharmaceutical company involved in the manufacture and sale of pharmaceutical products across South Korea, China, Japan, the United States, and other international markets, with a market cap of ₩3.75 trillion.

Operations: The company's revenue segments consist of Medicine at ₩1.13 trillion, Overseas Medicine at ₩354.39 billion, and Raw Drug Substance at ₩106.89 billion.

Estimated Discount To Fair Value: 39.4%

Hanmi Pharm is trading at ₩296,000, significantly below its estimated fair value of ₩488,229.59, indicating a potential undervaluation. The company anticipates robust earnings growth of 21.8% annually over the next three years, outpacing the Korean market's average. Despite a lower forecasted return on equity of 13.9%, Hanmi Pharm’s revenue is expected to grow faster than the market at 8.4% per year, supporting its strong cash flow position amidst recent earnings fluctuations.

- In light of our recent growth report, it seems possible that Hanmi Pharm's financial performance will exceed current levels.

- Click here to discover the nuances of Hanmi Pharm with our detailed financial health report.

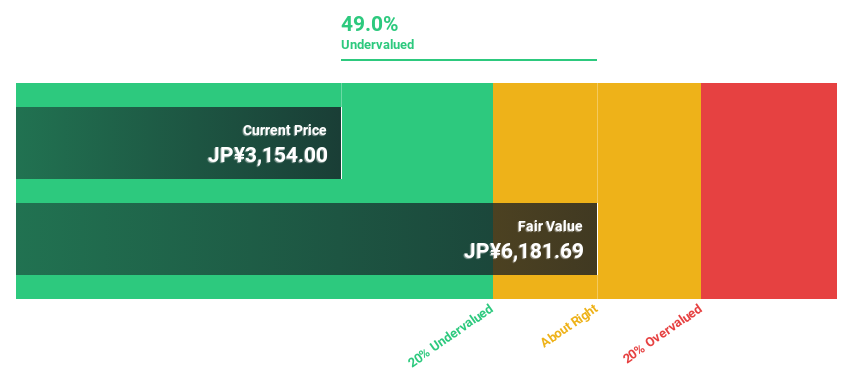

GMO internet group (TSE:9449)

Overview: GMO Internet Group, Inc. offers a range of internet services globally and has a market capitalization of approximately ¥378.28 billion.

Operations: The company's revenue segments include Internet Infrastructure, Online Advertising & Media, Internet Finance, and Cryptoassets.

Estimated Discount To Fair Value: 41.1%

GMO Internet Group is trading at ¥3,719, significantly below its estimated fair value of ¥6,316.09, highlighting a potential undervaluation. The company's earnings are projected to grow at 16.9% annually, surpassing the Japanese market's average growth rate of 7.7%. Additionally, revenue growth is expected to outpace the market at 7.9% per year. Recent buybacks and dividend increases reflect a commitment to shareholder returns while maintaining strong cash flow management amidst moderate profit growth expectations.

- Upon reviewing our latest growth report, GMO internet group's projected financial performance appears quite optimistic.

- Click to explore a detailed breakdown of our findings in GMO internet group's balance sheet health report.

Key Takeaways

- Explore the 253 names from our Undervalued Asian Stocks Based On Cash Flows screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A007660

ISU Petasys

Manufactures and sells printed circuit boards (PCBs) worldwide.

Outstanding track record with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.9% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.1% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|36.0% overvalued

DA

Community Contributor