- South Korea

- /

- Electronic Equipment and Components

- /

- KOSE:A006400

Will Weakness in Samsung SDI Co., Ltd.'s (KRX:006400) Stock Prove Temporary Given Strong Fundamentals?

It is hard to get excited after looking at Samsung SDI's (KRX:006400) recent performance, when its stock has declined 7.3% over the past month. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. Particularly, we will be paying attention to Samsung SDI's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for Samsung SDI

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Samsung SDI is:

9.2% = ₩1.9t ÷ ₩21t (Based on the trailing twelve months to March 2024).

The 'return' is the yearly profit. That means that for every ₩1 worth of shareholders' equity, the company generated ₩0.09 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

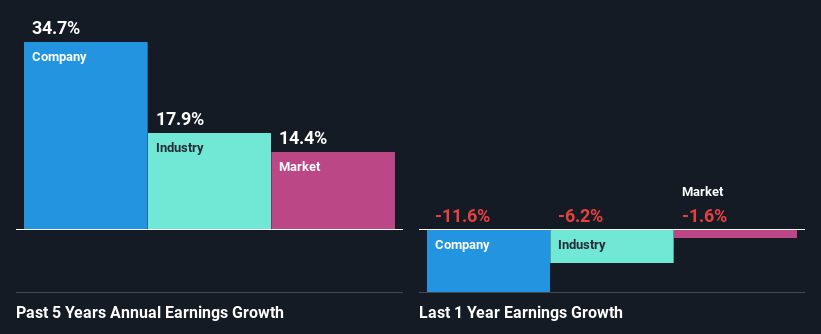

A Side By Side comparison of Samsung SDI's Earnings Growth And 9.2% ROE

When you first look at it, Samsung SDI's ROE doesn't look that attractive. However, the fact that the its ROE is quite higher to the industry average of 7.3% doesn't go unnoticed by us. Especially when you consider Samsung SDI's exceptional 35% net income growth over the past five years. That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. Therefore, the growth in earnings could also be the result of other factors. For example, it is possible that the broader industry is going through a high growth phase, or that the company has a low payout ratio.

Next, on comparing with the industry net income growth, we found that Samsung SDI's growth is quite high when compared to the industry average growth of 18% in the same period, which is great to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Samsung SDI is trading on a high P/E or a low P/E, relative to its industry.

Is Samsung SDI Efficiently Re-investing Its Profits?

Samsung SDI's three-year median payout ratio to shareholders is 3.9%, which is quite low. This implies that the company is retaining 96% of its profits. So it looks like Samsung SDI is reinvesting profits heavily to grow its business, which shows in its earnings growth.

Besides, Samsung SDI has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to drop to 2.8% over the next three years. The fact that the company's ROE is expected to rise to 12% over the same period is explained by the drop in the payout ratio.

Conclusion

In total, we are pretty happy with Samsung SDI's performance. Particularly, we like that the company is reinvesting heavily into its business at a moderate rate of return. Unsurprisingly, this has led to an impressive earnings growth. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A006400

Samsung SDI

Manufactures and sells batteries in South Korea, Europe, China, North America, Southeast Asia, and internationally.

Undervalued with moderate growth potential.