- South Korea

- /

- IT

- /

- KOSE:A307950

Hyundai Autoever Corporation's (KRX:307950) Business Is Yet to Catch Up With Its Share Price

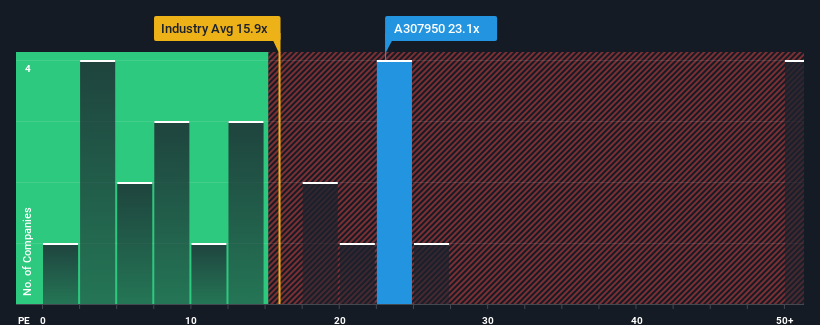

When close to half the companies in Korea have price-to-earnings ratios (or "P/E's") below 10x, you may consider Hyundai Autoever Corporation (KRX:307950) as a stock to avoid entirely with its 23.1x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for Hyundai Autoever as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Hyundai Autoever

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Hyundai Autoever would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings growth, the company posted a worthy increase of 3.5%. Pleasingly, EPS has also lifted 103% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 24% during the coming year according to the analysts following the company. That's shaping up to be materially lower than the 34% growth forecast for the broader market.

With this information, we find it concerning that Hyundai Autoever is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Bottom Line On Hyundai Autoever's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Hyundai Autoever's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Hyundai Autoever with six simple checks.

Of course, you might also be able to find a better stock than Hyundai Autoever. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Hyundai Autoever might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A307950

Hyundai Autoever

Provides information and communication technology services in South Korea and internationally.

Excellent balance sheet and good value.

Market Insights

Community Narratives