Advertisement

- China

- /

- Real Estate

- /

- SZSE:000573

Undiscovered Gems Three Stocks To Watch In November 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the shifting landscape of policy changes under the new U.S. administration, small-cap stocks have experienced notable volatility, with indices like the Russell 2000 reflecting a cautious investor sentiment. Amidst this backdrop of economic uncertainty and sector-specific fluctuations, identifying promising opportunities requires a keen eye for companies that demonstrate resilience and potential for growth in turbulent times.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Brillian Network & Automation Integrated System | 8.39% | 20.15% | 19.93% | ★★★★★★ |

| Arab Insurance Group (B.S.C.) | NA | -59.46% | 20.33% | ★★★★★★ |

| Parker Drilling | 46.25% | -0.33% | 53.04% | ★★★★★★ |

| Gallant Precision Machining | 29.51% | -2.07% | 4.51% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Song Hong Garment | 62.50% | 3.80% | -5.84% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Hankook (KOSE:A000240)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hankook & Company Co., Ltd. is engaged in the manufacturing and selling of storage batteries, with a market cap of ₩1.61 trillion.

Operations: Hankook & Company Co., Ltd. generates revenue primarily through the manufacturing and sale of storage batteries.

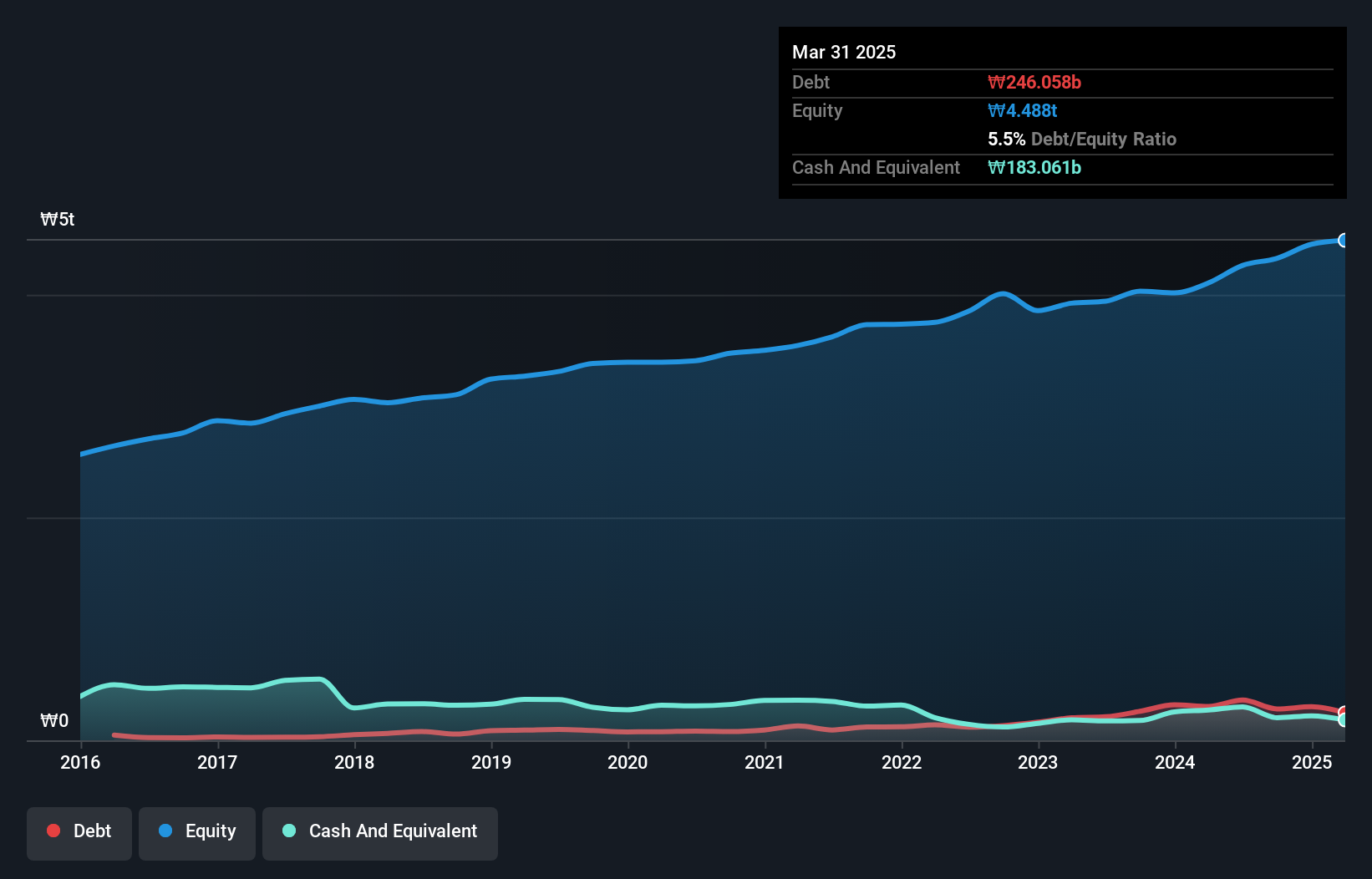

Hankook, a promising player in the auto components sector, showcases impressive earnings growth of 240% over the past year, outpacing industry averages. Trading at 83.6% below its estimated fair value suggests potential for investors seeking undervalued opportunities. The company's net debt to equity ratio stands at a satisfactory 1.8%, indicating prudent financial management despite an increase from 2.6% to 6.5% over five years. Recent results highlight robust performance with third-quarter sales reaching KRW 5,947 million and net income of KRW 120,683 million, reflecting substantial progress compared to last year's figures.

- Dive into the specifics of Hankook here with our thorough health report.

Gain insights into Hankook's historical performance by reviewing our past performance report.

KCTech (KOSE:A281820)

Simply Wall St Value Rating: ★★★★★★

Overview: KCTech Co., Ltd. operates in South Korea, focusing on the manufacture and distribution of semiconductor systems, display systems, and electronic materials, with a market cap of approximately ₩645.67 billion.

Operations: KCTech generates revenue primarily through its semiconductor systems, display systems, and electronic materials segments. The company has a market cap of approximately ₩645.67 billion.

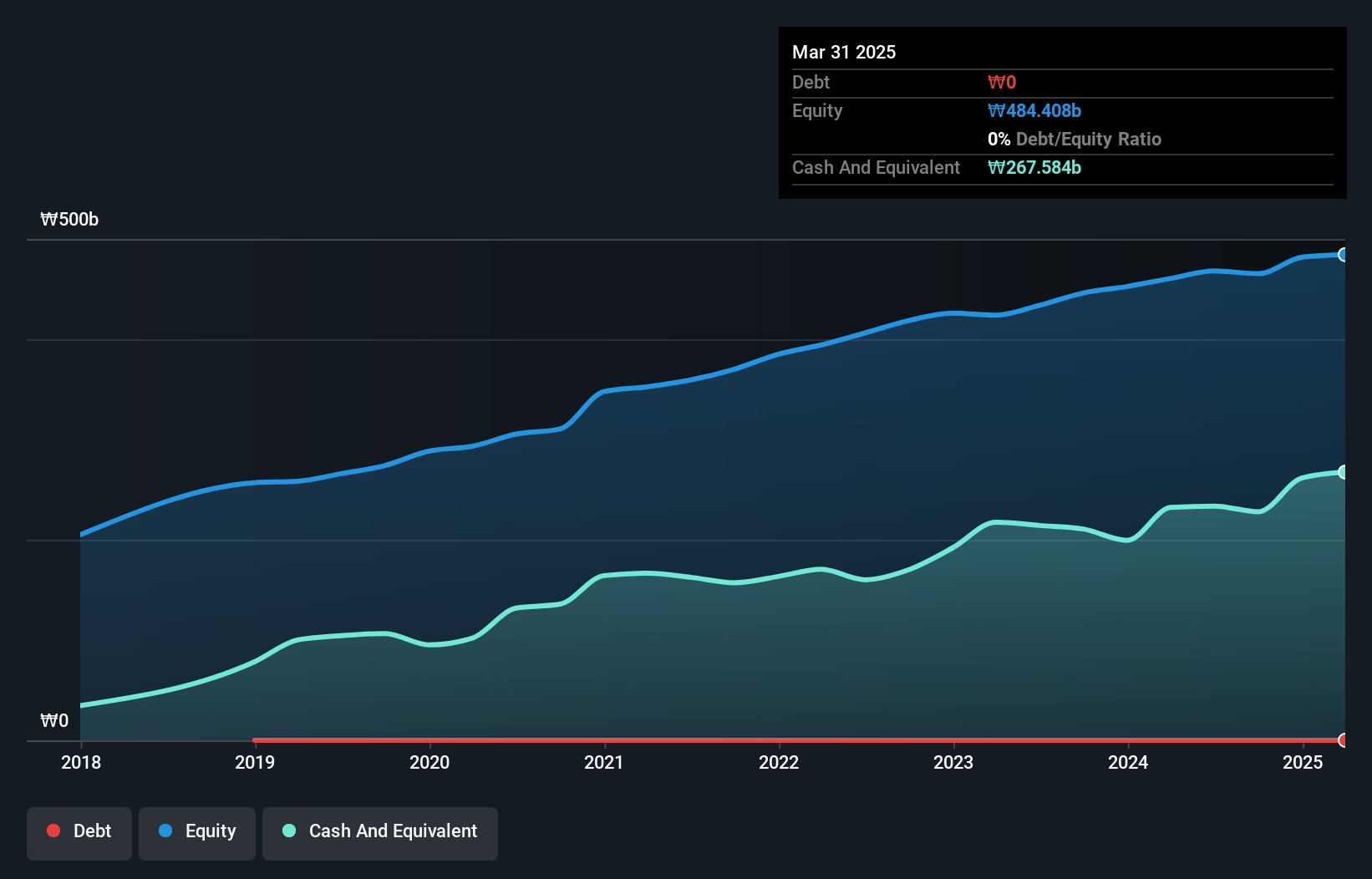

KCTech stands out with its robust financial health, being debt-free for the past five years and boasting high-quality earnings. Despite a slight negative earnings growth of 1.5% over the past year, it still outpaced the Semiconductor industry's average decline of 7.6%. The company is set to enhance shareholder value through a share repurchase program worth KRW 10 billion, aiming to stabilize stock prices by March 2025. With positive free cash flow and forecasted annual earnings growth of 24.54%, KCTech seems well-positioned for future expansion in its niche market segment.

- Navigate through the intricacies of KCTech with our comprehensive health report here.

Explore historical data to track KCTech's performance over time in our Past section.

DongGuan Winnerway Industry Zone (SZSE:000573)

Simply Wall St Value Rating: ★★★★☆☆

Overview: DongGuan Winnerway Industry Zone LTD. operates in the real estate development sector in China, with a market capitalization of approximately CN¥1.87 billion.

Operations: Winnerway Industry Zone derives its revenue primarily from real estate development activities. Its financial performance is influenced by various cost factors inherent in the real estate sector. The company's net profit margin has shown variability, reflecting changes in operational efficiency and market conditions over time.

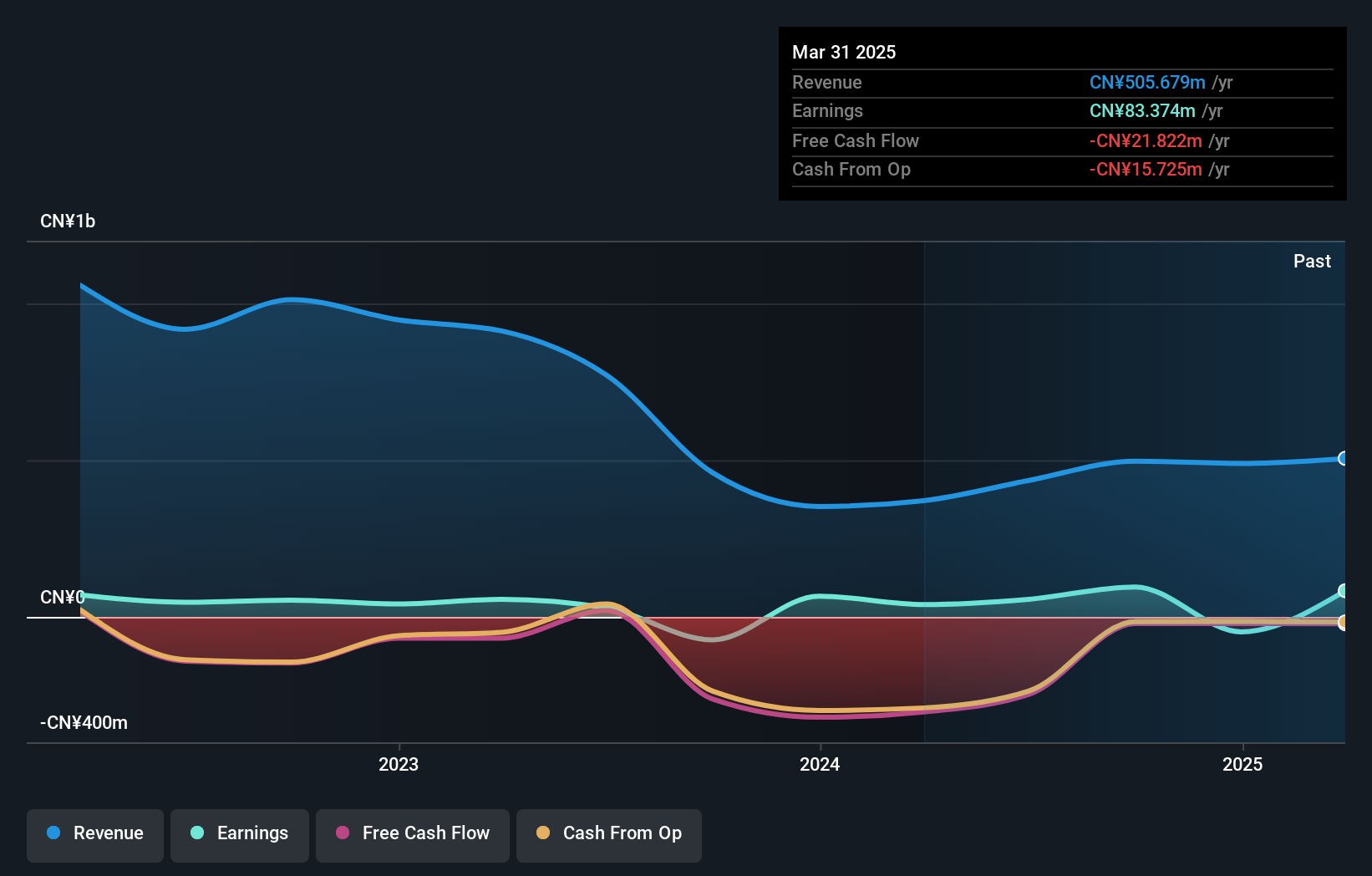

DongGuan Winnerway Industry Zone, a smaller player in its field, has shown notable progress with sales reaching CNY 416.83 million for the first nine months of 2024, up from CNY 272.08 million last year. Despite reporting a net loss of CNY 38.76 million, this is an improvement compared to the previous year's loss of CNY 68.31 million. The company seems to be navigating financial challenges well, as evidenced by its reduced debt-to-equity ratio from 40.6% to 20.7% over five years and maintaining more cash than total debt, indicating sound financial management amidst industry hurdles.

Key Takeaways

- Embark on your investment journey to our 4638 Undiscovered Gems With Strong Fundamentals selection here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:000573

DongGuan Winnerway Industry Zone

Engages in the real estate development business in China.

Adequate balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor