- South Korea

- /

- Semiconductors

- /

- KOSE:A000990

1.7% earnings growth over 3 years has not materialized into gains for DB HiTek (KRX:000990) shareholders over that period

If you are building a properly diversified stock portfolio, the chances are some of your picks will perform badly. But long term DB HiTek CO., LTD. (KRX:000990) shareholders have had a particularly rough ride in the last three year. Sadly for them, the share price is down 58% in that time. And more recent buyers are having a tough time too, with a drop of 38% in the last year. Furthermore, it's down 19% in about a quarter. That's not much fun for holders.

Since DB HiTek has shed ₩145b from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

Check out our latest analysis for DB HiTek

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

During the unfortunate three years of share price decline, DB HiTek actually saw its earnings per share (EPS) improve by 5.1% per year. This is quite a puzzle, and suggests there might be something temporarily buoying the share price. Or else the company was over-hyped in the past, and so its growth has disappointed.

Since the change in EPS doesn't seem to correlate with the change in share price, it's worth taking a look at other metrics.

The modest 1.9% dividend yield is unlikely to be guiding the market view of the stock. Arguably the revenue decline of 5.2% per year has people thinking DB HiTek is shrinking. And that's not surprising, since it seems unlikely that EPS growth can continue for long in the absence of revenue growth.

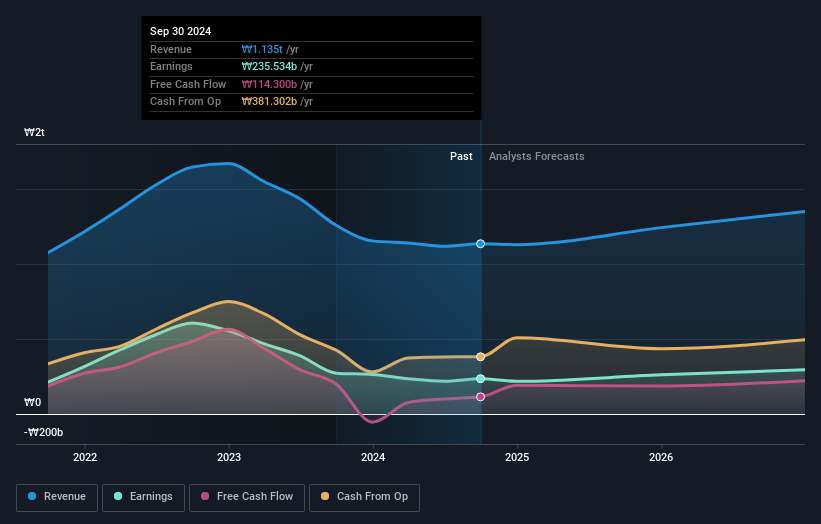

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

This free interactive report on DB HiTek's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

We regret to report that DB HiTek shareholders are down 38% for the year (even including dividends). Unfortunately, that's worse than the broader market decline of 3.9%. Having said that, it's inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. On the bright side, long term shareholders have made money, with a gain of 2% per year over half a decade. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Even so, be aware that DB HiTek is showing 1 warning sign in our investment analysis , you should know about...

Of course DB HiTek may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on South Korean exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A000990

DB HiTek

DB HiTek Co.,Ltd. engages in semiconductor foundry business in South Korea.

Very undervalued with flawless balance sheet.

Market Insights

Community Narratives