- South Korea

- /

- Semiconductors

- /

- KOSDAQ:A046890

Seoul Semiconductor Co., Ltd. (KOSDAQ:046890) Looks Inexpensive After Falling 25% But Perhaps Not Attractive Enough

The Seoul Semiconductor Co., Ltd. (KOSDAQ:046890) share price has fared very poorly over the last month, falling by a substantial 25%. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 29% in that time.

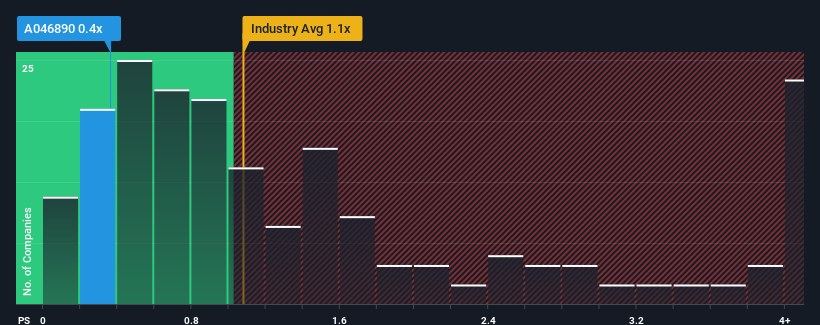

Since its price has dipped substantially, it would be understandable if you think Seoul Semiconductor is a stock with good investment prospects with a price-to-sales ratios (or "P/S") of 0.4x, considering almost half the companies in Korea's Semiconductor industry have P/S ratios above 1.1x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Seoul Semiconductor

What Does Seoul Semiconductor's Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, Seoul Semiconductor has been relatively sluggish. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Seoul Semiconductor.What Are Revenue Growth Metrics Telling Us About The Low P/S?

The only time you'd be truly comfortable seeing a P/S as low as Seoul Semiconductor's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a decent 8.9% gain to the company's revenues. However, this wasn't enough as the latest three year period has seen an unpleasant 16% overall drop in revenue. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 1.3% during the coming year according to the five analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 48%, which is noticeably more attractive.

With this information, we can see why Seoul Semiconductor is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

The southerly movements of Seoul Semiconductor's shares means its P/S is now sitting at a pretty low level. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As expected, our analysis of Seoul Semiconductor's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Seoul Semiconductor that you should be aware of.

If you're unsure about the strength of Seoul Semiconductor's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A046890

Seoul Semiconductor

Manufactures and sells light emitting diodes (LEDs) products worldwide.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives