- South Korea

- /

- Pharma

- /

- KOSE:A003850

Undiscovered Gems With Promising Potential For December 2024

Reviewed by Simply Wall St

As global markets navigate a landscape marked by interest rate cuts from the ECB and SNB, alongside expectations for a Federal Reserve rate reduction, small-cap stocks have faced challenges, with the Russell 2000 Index underperforming against larger peers like the S&P 500. In this environment of cautious optimism and shifting monetary policies, identifying stocks with strong fundamentals and growth potential becomes crucial for investors seeking opportunities in lesser-known companies.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Hong Tai Electric Industrial | 0.03% | 11.52% | 12.52% | ★★★★★★ |

| C&D Property Management Group | 1.32% | 37.15% | 41.55% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Pacific Construction | 21.40% | -3.50% | 26.25% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Lion Travel Service | 1.97% | -0.25% | 46.60% | ★★★★★☆ |

| Central Finance | 1.16% | 10.03% | 16.10% | ★★★★★☆ |

| Huang Hsiang Construction | 266.70% | 13.12% | 15.19% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

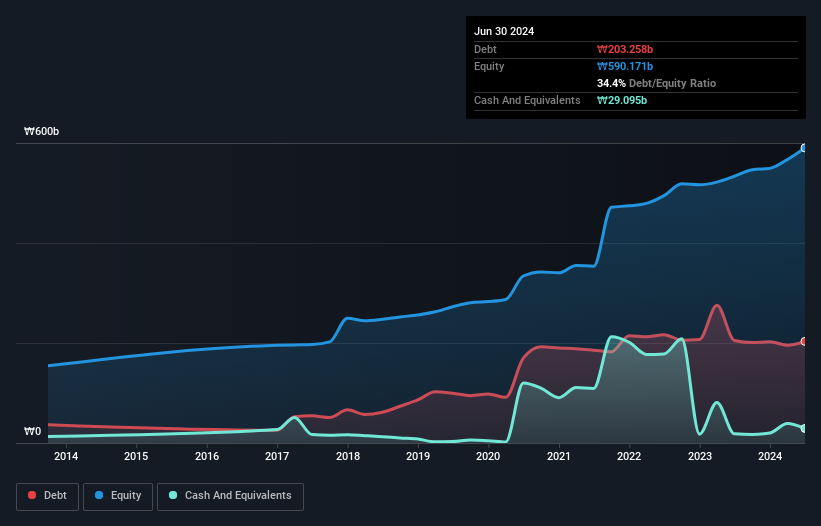

Boryung (KOSE:A003850)

Simply Wall St Value Rating: ★★★★★★

Overview: Boryung Corporation is involved in the manufacture and sale of pharmaceutical products both in South Korea and internationally, with a market capitalization of ₩675.78 billion.

Operations: Boryung Corporation's primary revenue stream is from pharmaceutical manufacturing and sales, generating approximately ₩991.43 billion.

Boryung seems to be carving a niche in the pharmaceuticals industry with its robust earnings growth of 119% over the past year, outpacing the industry's 22%. Trading at a price-to-earnings ratio of 10.9x, it offers good value compared to the KR market average of 11.4x. The company has successfully reduced its debt-to-equity ratio from 33.8% to 30.4% over five years, indicating prudent financial management. A recent private placement raised approximately ₩175 billion (US$), suggesting strategic capital allocation for future endeavors while maintaining a satisfactory net debt-to-equity ratio of 25.8%.

- Dive into the specifics of Boryung here with our thorough health report.

Review our historical performance report to gain insights into Boryung's's past performance.

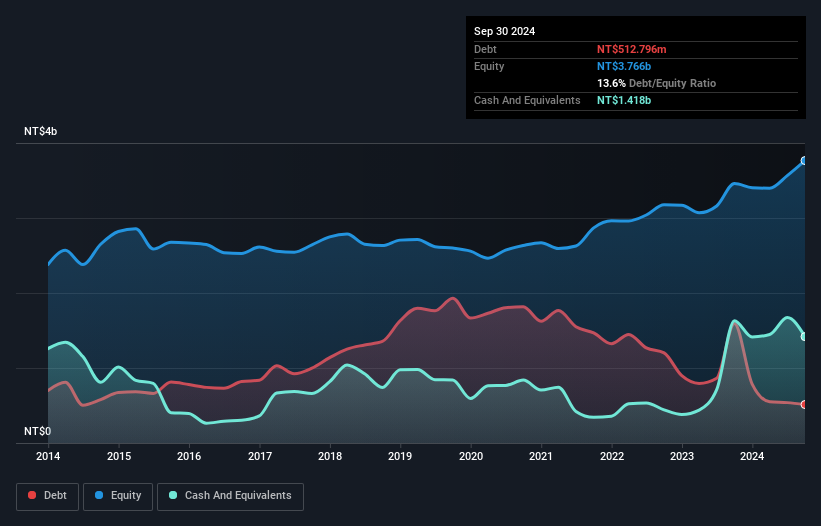

U.D. Electronic (TPEX:3689)

Simply Wall St Value Rating: ★★★★★★

Overview: U.D. Electronic Corp. engages in the research, manufacturing, and sale of electronic components and materials, connectors, and products primarily in Taiwan and China with a market capitalization of approximately NT$8.26 billion.

Operations: The company generates revenue primarily through the trading of signal connector manufacturing, amounting to NT$5.06 billion.

U.D. Electronic, a small player in the electronics sector, seems to be navigating some challenges and opportunities. Recently announced earnings show third-quarter sales at TWD 1.43 billion, down from TWD 1.77 billion last year, yet net income rose to TWD 186 million from TWD 162 million. Despite a volatile share price lately, the company has reduced its debt-to-equity ratio significantly over five years from 74% to just under 14%. With free cash flow positive and trading well below estimated fair value by nearly 80%, U.D.'s financial health appears robust despite recent shareholder dilution concerns.

- Click here and access our complete health analysis report to understand the dynamics of U.D. Electronic.

Understand U.D. Electronic's track record by examining our Past report.

Kernel Holding (WSE:KER)

Simply Wall St Value Rating: ★★★★★★

Overview: Kernel Holding S.A. operates a diversified agricultural business with activities across India, Hong Kong, China, Singapore, Switzerland, the Netherlands, Ukraine, Spain, and other international markets; it has a market cap of PLN3.87 billion.

Operations: Kernel Holding generates revenue primarily from its Infrastructure and Trading segment at $2.16 billion, followed by Oilseed Processing at $1.86 billion, and Farming at $565.45 million. The company incurs a negative reconciliation of -$746.04 million in its financial reporting.

Kernel Holding, a relatively small player in its sector, has faced significant challenges recently. The company reported a net income of US$167.95 million for the fiscal year ending June 2024, down from US$299.19 million the previous year, partly due to a one-off loss of US$161.9 million impacting results up to September 2024. Despite this setback, Kernel's earnings grew by an impressive 198% over the past year, outpacing industry growth of 39%. However, concerns remain as auditors have expressed doubts about its ability to continue as a going concern. On the financial side, Kernel's debt-to-equity ratio improved from 61% to 48% over five years and interest payments are well covered by EBIT at a multiple of twelve times.

- Delve into the full analysis health report here for a deeper understanding of Kernel Holding.

Assess Kernel Holding's past performance with our detailed historical performance reports.

Where To Now?

- Unlock more gems! Our Undiscovered Gems With Strong Fundamentals screener has unearthed 4622 more companies for you to explore.Click here to unveil our expertly curated list of 4625 Undiscovered Gems With Strong Fundamentals.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Boryung might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A003850

Boryung

Engages in the manufacture and sale of pharmaceutical products in South Korea and internationally.

Flawless balance sheet with solid track record.

Market Insights

Community Narratives