- South Korea

- /

- Pharma

- /

- KOSE:A003220

Daewon Pharmaceutical Co., Ltd.'s (KRX:003220) Stock Has Shown Weakness Lately But Financial Prospects Look Decent: Is The Market Wrong?

With its stock down 10% over the past month, it is easy to disregard Daewon Pharmaceutical (KRX:003220). However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. Particularly, we will be paying attention to Daewon Pharmaceutical's ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for Daewon Pharmaceutical

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Daewon Pharmaceutical is:

11% = ₩24b ÷ ₩209b (Based on the trailing twelve months to September 2020).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every ₩1 worth of equity, the company was able to earn ₩0.11 in profit.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

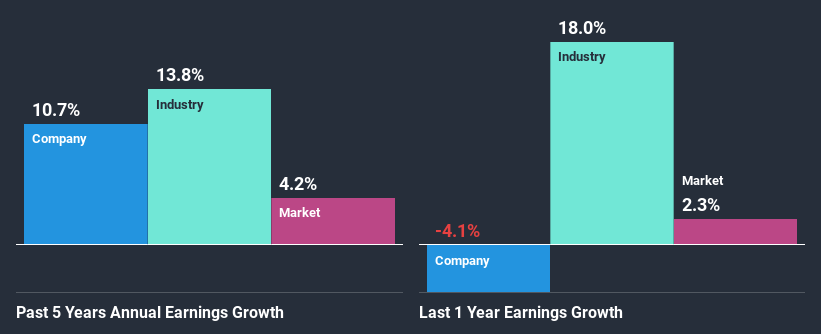

Daewon Pharmaceutical's Earnings Growth And 11% ROE

At first glance, Daewon Pharmaceutical's ROE doesn't look very promising. However, the fact that the its ROE is quite higher to the industry average of 7.6% doesn't go unnoticed by us. Consequently, this likely laid the ground for the decent growth of 11% seen over the past five years by Daewon Pharmaceutical. That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. So there might well be other reasons for the earnings to grow. For example, it is possible that the broader industry is going through a high growth phase, or that the company has a low payout ratio.

As a next step, we compared Daewon Pharmaceutical's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 14% in the same period.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. Is Daewon Pharmaceutical fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Daewon Pharmaceutical Efficiently Re-investing Its Profits?

Daewon Pharmaceutical has a low three-year median payout ratio of 20%, meaning that the company retains the remaining 80% of its profits. This suggests that the management is reinvesting most of the profits to grow the business.

Besides, Daewon Pharmaceutical has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders.

Conclusion

On the whole, we do feel that Daewon Pharmaceutical has some positive attributes. In particular, it's great to see that the company is investing heavily into its business and along with a moderate rate of return, that has resulted in a respectable growth in its earnings.

If you decide to trade Daewon Pharmaceutical, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A003220

Daewon Pharmaceutical

A pharmaceutical company, manufactures and sells medicines and medical supplies in South Korea.

Good value with reasonable growth potential.