- South Korea

- /

- Personal Products

- /

- KOSDAQ:A241710

KRX Stocks Priced Below Estimated Value In October 2024

Reviewed by Simply Wall St

In the last week, the South Korean market has remained flat, yet it has experienced a 3.8% increase over the past year, with earnings anticipated to grow by 30% annually in the coming years. In this context of steady growth and promising future earnings, identifying stocks that are priced below their estimated value can present compelling opportunities for investors seeking to capitalize on potential market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In South Korea

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| T'Way Air (KOSE:A091810) | ₩2940.00 | ₩5544.03 | 47% |

| PharmaResearch (KOSDAQ:A214450) | ₩225000.00 | ₩424282.09 | 47% |

| Sejin Heavy Industries (KOSE:A075580) | ₩7390.00 | ₩14743.96 | 49.9% |

| Cosmecca Korea (KOSDAQ:A241710) | ₩77700.00 | ₩147702.09 | 47.4% |

| TSE (KOSDAQ:A131290) | ₩53300.00 | ₩99749.67 | 46.6% |

| Lutronic (KOSDAQ:A085370) | ₩36700.00 | ₩63217.94 | 41.9% |

| Shinsung E&GLtd (KOSE:A011930) | ₩1605.00 | ₩2941.18 | 45.4% |

| Global Tax Free (KOSDAQ:A204620) | ₩3830.00 | ₩6405.75 | 40.2% |

| Kakao Games (KOSDAQ:A293490) | ₩17220.00 | ₩29657.37 | 41.9% |

| Hotel ShillaLtd (KOSE:A008770) | ₩45850.00 | ₩76012.74 | 39.7% |

Here we highlight a subset of our preferred stocks from the screener.

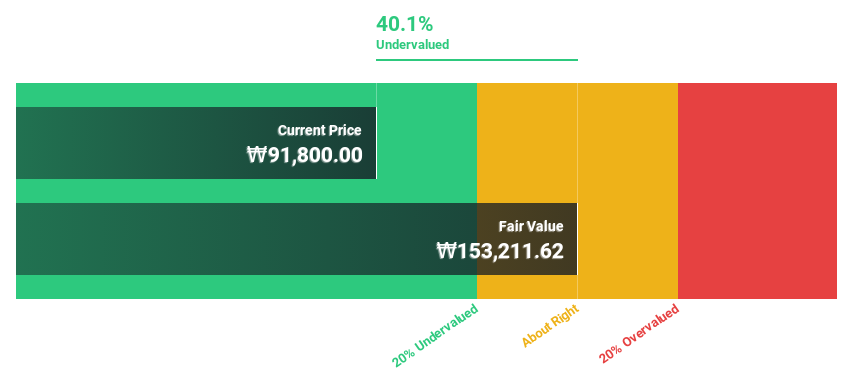

ST PharmLtd (KOSDAQ:A237690)

Overview: ST Pharm Co., Ltd. offers custom manufacturing services for active pharmaceutical ingredients and intermediates both in South Korea and internationally, with a market cap of ₩2.19 trillion.

Operations: ST Pharm Co., Ltd. generates revenue through its Raw Material Manufacturing segment, contributing ₩236.78 billion, and the Clinical Trial Site Consignment Research Institute, which adds ₩36.38 billion.

Estimated Discount To Fair Value: 26.8%

ST Pharm Ltd. is trading at ₩109,100, significantly below its estimated fair value of ₩148,993.44, making it highly undervalued based on discounted cash flow analysis. Despite recent shareholder dilution and share price volatility, the company's earnings have grown 67.5% annually over the past five years and are forecast to grow 37.36% per year going forward—outpacing the Korean market's expected growth rate of 30.3%.

- Insights from our recent growth report point to a promising forecast for ST PharmLtd's business outlook.

- Unlock comprehensive insights into our analysis of ST PharmLtd stock in this financial health report.

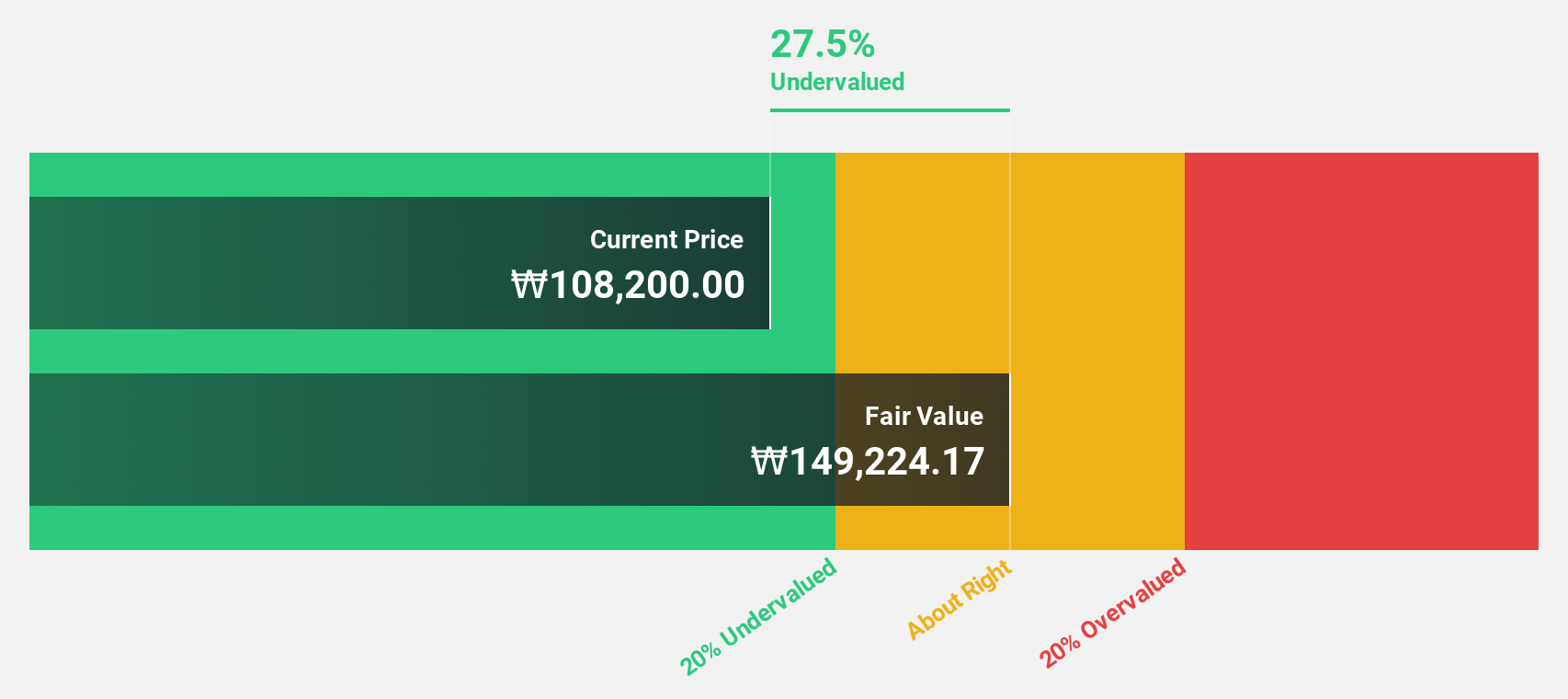

Cosmecca Korea (KOSDAQ:A241710)

Overview: Cosmecca Korea Co., Ltd. is involved in the research, development, manufacture, and sale of skincare products both in South Korea and internationally, with a market cap of ₩829.84 billion.

Operations: The company's revenue is primarily derived from cosmetics, amounting to ₩558.96 billion, along with a smaller contribution from technology fees totaling ₩3.17 billion.

Estimated Discount To Fair Value: 47.4%

Cosmecca Korea is trading at ₩77,700, significantly below its estimated fair value of ₩147,702.09, indicating a strong undervaluation based on discounted cash flow analysis. The company's revenue is projected to grow 14.8% annually, surpassing the Korean market's expected growth of 10.4%. However, its earnings growth forecast of 21.6% per year lags behind the market's anticipated rate of 30.3%, despite a notable past year's profit increase of over 200%.

- Our growth report here indicates Cosmecca Korea may be poised for an improving outlook.

- Dive into the specifics of Cosmecca Korea here with our thorough financial health report.

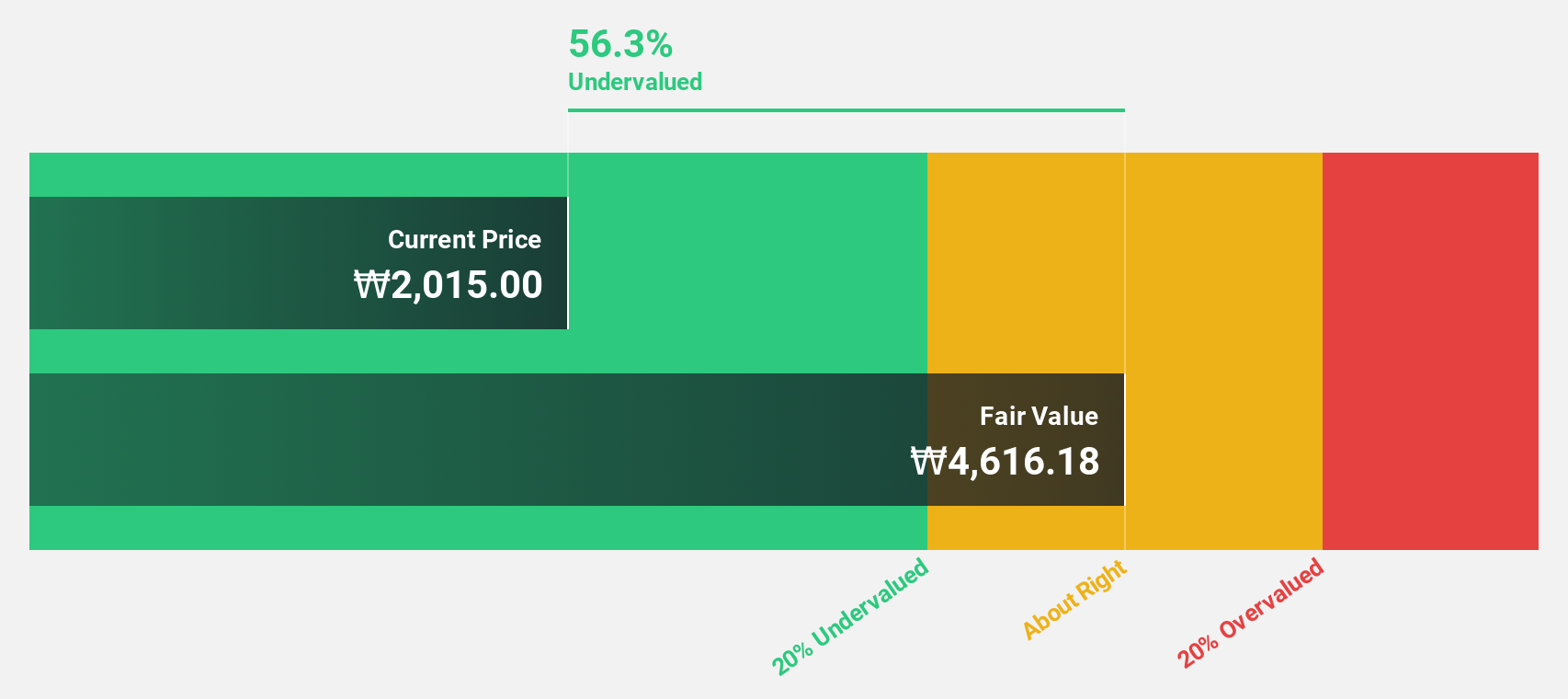

T'Way Air (KOSE:A091810)

Overview: T'Way Air Co., Ltd. offers air transportation services both within South Korea and internationally, with a market cap of ₩632.61 billion.

Operations: The company's revenue primarily comes from its Aviation Business segment, which generated ₩1.45 billion.

Estimated Discount To Fair Value: 47%

T'Way Air, trading at ₩2,940, is significantly undervalued compared to its estimated fair value of ₩5,544.03 according to discounted cash flow analysis. Despite recent shareholder dilution and high share price volatility, earnings are projected to grow 23.39% annually over the next three years. The company's revenue growth forecast of 11.1% per year outpaces the Korean market's average but trails behind in profit growth expectations relative to market benchmarks.

- Our expertly prepared growth report on T'Way Air implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of T'Way Air with our detailed financial health report.

Turning Ideas Into Actions

- Gain an insight into the universe of 35 Undervalued KRX Stocks Based On Cash Flows by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A241710

Cosmecca Korea

Engages in the research and development, manufacture, and sale of skincare products in South Korea and internationally.

Flawless balance sheet and undervalued.

Market Insights

Community Narratives