- South Korea

- /

- Pharma

- /

- KOSDAQ:A183490

There's Reason For Concern Over Enzychem Lifesciences Corporation's (KOSDAQ:183490) Price

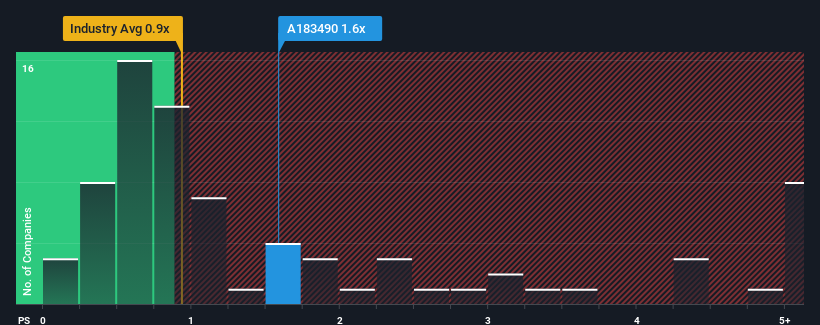

When you see that almost half of the companies in the Pharmaceuticals industry in Korea have price-to-sales ratios (or "P/S") below 0.9x, Enzychem Lifesciences Corporation (KOSDAQ:183490) looks to be giving off some sell signals with its 1.6x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for Enzychem Lifesciences

How Has Enzychem Lifesciences Performed Recently?

Recent times have been quite advantageous for Enzychem Lifesciences as its revenue has been rising very briskly. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. However, if this isn't the case, investors might get caught out paying too much for the stock.

Although there are no analyst estimates available for Enzychem Lifesciences, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Enzychem Lifesciences' to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 133% last year. The strong recent performance means it was also able to grow revenue by 284% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Weighing that recent medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 62% shows it's about the same on an annualised basis.

With this information, we find it interesting that Enzychem Lifesciences is trading at a high P/S compared to the industry. Apparently many investors in the company are more bullish than recent times would indicate and aren't willing to let go of their stock right now. Although, additional gains will be difficult to achieve as a continuation of recent revenue trends would weigh down the share price eventually.

What We Can Learn From Enzychem Lifesciences' P/S?

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our look into Enzychem Lifesciences has shown that it currently trades on a higher than expected P/S since its recent three-year growth is only in line with the wider industry forecast. Right now we are uncomfortable with the high P/S as this revenue performance isn't likely to support such positive sentiment for long. Unless there is a significant improvement in the company's medium-term trends, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Enzychem Lifesciences (1 is a bit unpleasant!) that you need to be mindful of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Enzychem Lifesciences might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A183490

Enzychem Lifesciences

Engages in developing novel small molecule therapeutics for patients with unmet needs for oncology, inflammatory, and severe respiratory diseases in South Korea.

Flawless balance sheet and overvalued.

Market Insights

Community Narratives