Advertisement

- South Korea

- /

- Biotech

- /

- KOSDAQ:A007390

We Think NatureCellLtd (KOSDAQ:007390) Can Easily Afford To Drive Business Growth

We can readily understand why investors are attracted to unprofitable companies. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

Given this risk, we thought we'd take a look at whether NatureCellLtd (KOSDAQ:007390) shareholders should be worried about its cash burn. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

View our latest analysis for NatureCellLtd

How Long Is NatureCellLtd's Cash Runway?

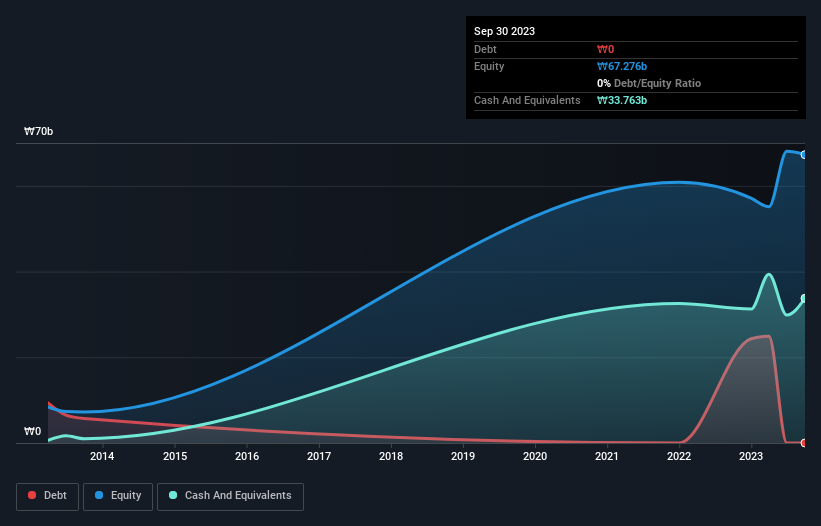

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. When NatureCellLtd last reported its September 2023 balance sheet in November 2023, it had zero debt and cash worth ₩34b. Looking at the last year, the company burnt through ₩3.5b. That means it had a cash runway of about 9.7 years as of September 2023. Even though this is but one measure of the company's cash burn, the thought of such a long cash runway warms our bellies in a comforting way. Depicted below, you can see how its cash holdings have changed over time.

How Well Is NatureCellLtd Growing?

NatureCellLtd managed to reduce its cash burn by 79% over the last twelve months, which suggests it's on the right flight path. And it could also show revenue growth of 3.3% in the same period. We think it is growing rather well, upon reflection. In reality, this article only makes a short study of the company's growth data. This graph of historic earnings and revenue shows how NatureCellLtd is building its business over time.

How Hard Would It Be For NatureCellLtd To Raise More Cash For Growth?

We are certainly impressed with the progress NatureCellLtd has made over the last year, but it is also worth considering how costly it would be if it wanted to raise more cash to fund faster growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Commonly, a business will sell new shares in itself to raise cash and drive growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

NatureCellLtd has a market capitalisation of ₩522b and burnt through ₩3.5b last year, which is 0.7% of the company's market value. So it could almost certainly just borrow a little to fund another year's growth, or else easily raise the cash by issuing a few shares.

How Risky Is NatureCellLtd's Cash Burn Situation?

As you can probably tell by now, we're not too worried about NatureCellLtd's cash burn. For example, we think its cash runway suggests that the company is on a good path. Its weak point is its revenue growth, but even that wasn't too bad! Taking all the factors in this report into account, we're not at all worried about its cash burn, as the business appears well capitalized to spend as needs be. An in-depth examination of risks revealed 1 warning sign for NatureCellLtd that readers should think about before committing capital to this stock.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

Valuation is complex, but we're here to simplify it.

Discover if NatureCellLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A007390

NatureCellLtd

Engages in manufacturing and selling of canned and health functional food products, beverages, stem cell, and cosmetics in South Korea.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.3% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|33.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|27.0% undervalued

MA

Community Contributor