Advertisement

- South Korea

- /

- Entertainment

- /

- KOSE:A352820

Statutory Profit Doesn't Reflect How Good HYBE's (KRX:352820) Earnings Are

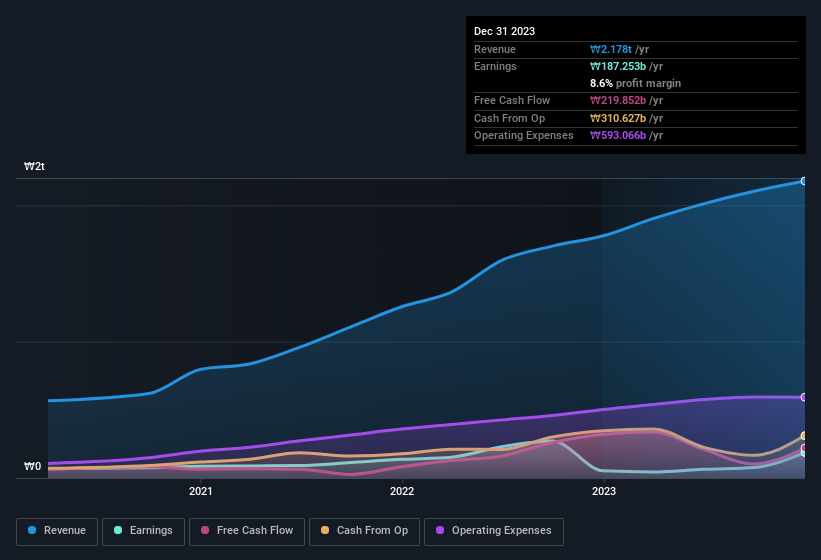

Even though HYBE Co., Ltd.'s (KRX:352820) recent earnings release was robust, the market didn't seem to notice. We think that investors have missed some encouraging factors underlying the profit figures.

See our latest analysis for HYBE

The Impact Of Unusual Items On Profit

For anyone who wants to understand HYBE's profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit was reduced by ₩137b due to unusual items. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. In the twelve months to December 2023, HYBE had a big unusual items expense. All else being equal, this would likely have the effect of making the statutory profit look worse than its underlying earnings power.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On HYBE's Profit Performance

As we mentioned previously, the HYBE's profit was hampered by unusual items in the last year. Because of this, we think HYBE's underlying earnings potential is as good as, or possibly even better, than the statutory profit makes it seem! Furthermore, it has done a great job growing EPS over the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you want to do dive deeper into HYBE, you'd also look into what risks it is currently facing. For example, we've discovered 1 warning sign that you should run your eye over to get a better picture of HYBE.

Today we've zoomed in on a single data point to better understand the nature of HYBE's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're here to simplify it.

Discover if HYBE might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A352820

HYBE

Engages in the music production, publishing, and artist development and management businesses.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|65.7% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.9% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.4% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.0% undervalued

AN

Based on Analyst Price Targets